Netflix: The DVD Business Was Never the Point

How a mail-order rental company made decisions that looked wrong at the time and built infrastructure competitors couldn't easily replicate.

In April 1998, Netflix launched as a DVD-by-mail service. You paid per rental, plus a small fee. The discs arrived in the mail. You watched them and sent them back. It was not an obvious disruption to anything.

Eighteen months later, in September 1999, the company switched models. For a flat monthly fee — initially around sixteen dollars — subscribers could hold up to three DVDs at a time, return them whenever they liked, and rent as many as they wanted. No due dates. No late fees.

At that moment, Netflix had a few hundred thousand subscribers. Blockbuster had roughly nine thousand stores, thirty million active customer accounts, and enough revenue from late fees alone to fund most of what Netflix was spending to exist. The competitive picture was not ambiguous.

What happened over the next eight years is usually told as a story about vision: Reed Hastings saw streaming coming, built a technology company in the guise of a DVD rental service, and outmaneuvered a complacent incumbent. That framing is satisfying, and it is largely wrong. Not because Hastings lacked foresight — he didn’t — but because the decisions that built Netflix’s structural position during the DVD era were not primarily acts of foresight. They were operational responses to immediate problems that accumulated structural value before anyone, including Netflix, fully recognized what was building. The streaming transition did not create that position. It inherited it.

The System

Netflix’s subscription model had a specific structural property that the per-rental model did not: it changed what the company needed to be good at.

In a per-rental business, revenue follows transactions. The better the selection of new releases, the more transactions. The better the store locations, the more transactions. Late fees were a secondary revenue line that required no additional capability — customers simply paid them when they kept discs too long, and the business collected.

In a subscription business, revenue follows retention. Every month a subscriber stays is a month of revenue that requires no additional transaction. Every month a subscriber cancels is revenue lost that requires an acquisition to replace. The operative variable is not how many discs get rented — it is how many subscribers stay. And subscribers stay when the product removes friction.

This shifted Netflix’s capital allocation logic entirely. Building more distribution centers was not a growth move — it was a retention move, because faster delivery meant subscribers got more value from their subscription and were less likely to cancel. Building a recommendation engine was not a technology indulgence — it was a retention move, because subscribers who found titles they actually wanted to watch used their subscription more and were less likely to cancel. Expanding the catalog was not a selection strategy — it was a retention move, because subscribers who could always find something worth watching did not conclude that Netflix had nothing left to offer them.

Each of these investments compounded the others. A subscriber who received fast delivery, had reliable recommendations, and could draw on a deep catalog was a subscriber with few reasons to leave. Each subscriber who stayed added another month of behavioral data to the recommendation engine. Each investment in delivery speed reduced churn, which reduced the cost of revenue.

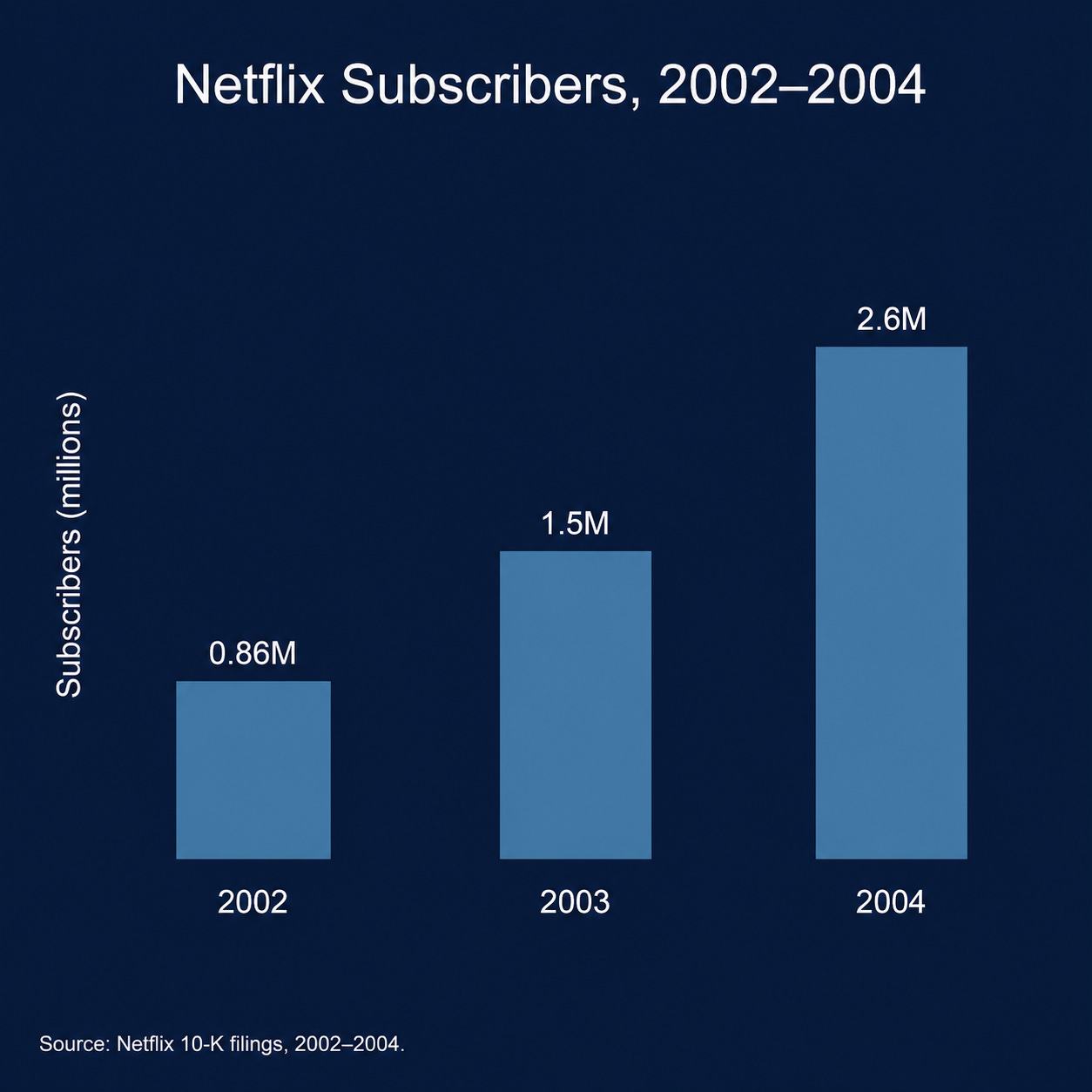

The model required a growing subscriber base to function at the unit economics it needed. That too was accumulating: 857,000 subscribers at year-end 2002, 1.5 million by the end of 2003, 2.6 million by the end of 2004.

In 2000, Netflix approached Blockbuster about an acquisition. Blockbuster declined. Netflix was burning cash at the time, the subscriber base was small, and the outcome was not a foregone conclusion.

The structural value was not in the subscriber count. It was in the relationship.

The Shift

In August 2004, Blockbuster launched Blockbuster Online. It was a direct response to Netflix — subscription model, DVD-by-mail, flat monthly fee. Within a year, Blockbuster Online had grown to more than 750,000 subscribers. It added an in-store exchange privilege that Netflix could not match: subscribers could return DVDs to a physical store and receive a new rental immediately, without waiting for the mail cycle.

This was a genuine competitive threat, and Blockbuster’s leadership recognized it as such. John Antioco, Blockbuster’s chairman and chief executive officer, described the company’s strategy in its Q4 2004 earnings call as an effort to “build on the initial success of Blockbuster Online” and address what he acknowledged was a declining in-store rental industry.

The problem was not the strategy. The problem was what executing the strategy required Blockbuster to do to itself.

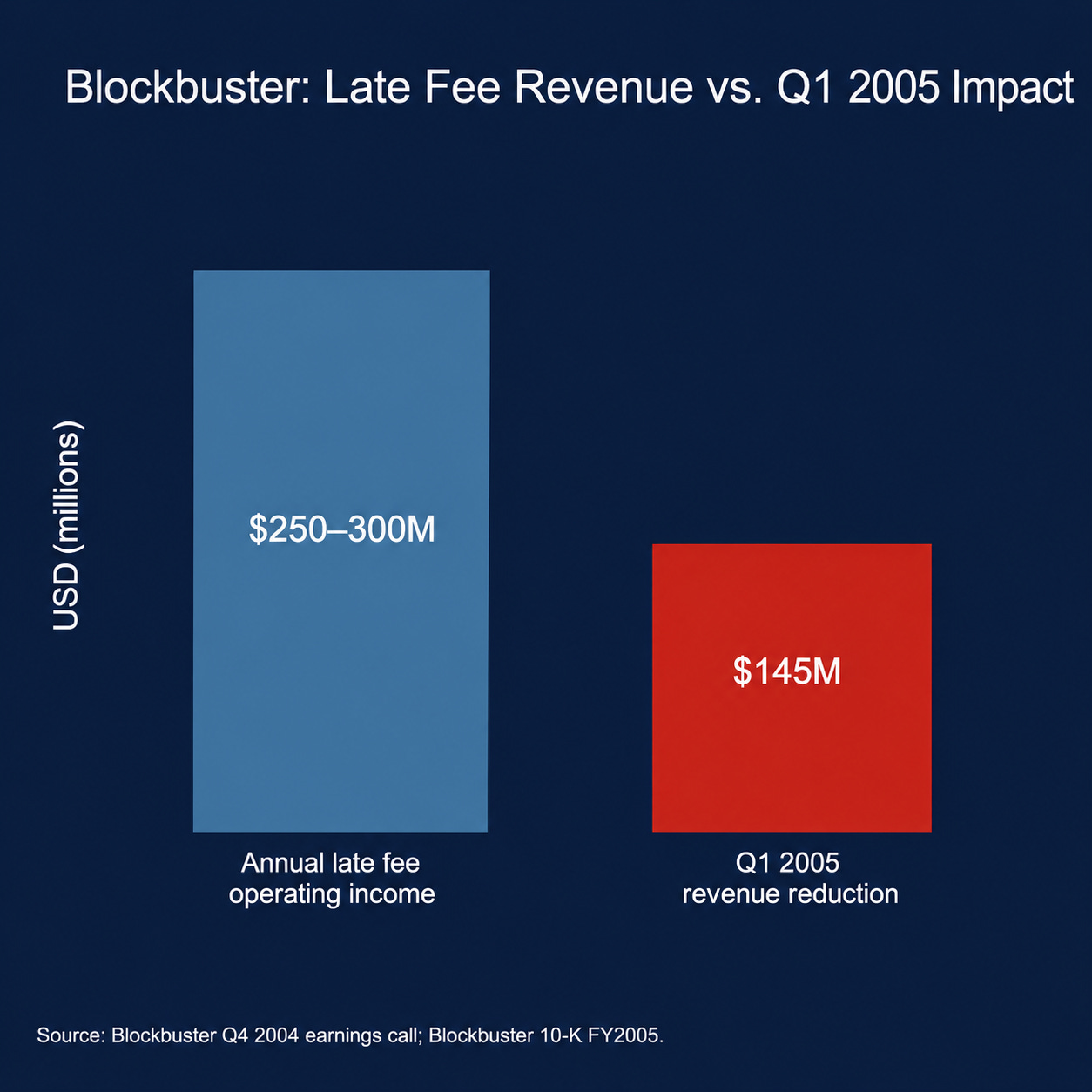

Blockbuster’s revenue model ran on late fees. At the Q4 2004 earnings call, Antioco acknowledged that late fees — which Blockbuster called “extended viewing fees” — had contributed approximately $250 to $300 million to the company’s operating income in 2004. He described the decision to eliminate them as “a lot of cash flow to offset and obviously a very serious decision.”

In January 2005, Blockbuster launched its No Late Fees program nationally. In the first quarter of 2005 alone, the elimination of extended viewing fee revenues reduced rental revenues by approximately $145 million. Blockbuster partially offset this through growth in base rental transactions — the No Late Fees program genuinely drove traffic — but the revenue model had been structurally altered in a way that required sustained volume growth to compensate for a lost revenue line that had required no volume at all.

Netflix reduced its monthly subscription price from $19.99 to $17.99 in October 2004, the same quarter Blockbuster Online launched. The price reduction cost Netflix revenue per subscriber. But Netflix was competing on a retention model where acquisition cost was the relevant variable, not operating income from a passive fee.

The Response

Blockbuster Online was not a halfhearted effort. Over the course of 2004 and 2005, Blockbuster invested approximately $140 million in capital expenditures and $120 million in operating costs to build the online subscription business and related initiatives. By the third quarter of 2005, Blockbuster Online had reached one million subscribers.

Netflix, at the same point, had approximately four million subscribers and was building toward profitability on a subscriber base it had been retaining for five years.

Blockbuster Online’s challenge was not execution — it was starting position. Building a distribution center network competitive with Netflix’s required years of iteration that Netflix had already completed. Building a recommendation system required behavioral data at the scale that Netflix had been accumulating since 2000. The in-store exchange privilege was a genuine differentiator, but it was also structurally tied to the retail cost structure that made the revenue sacrifices unsustainable.

The No Late Fees policy reversal later in 2005 captured the structural problem cleanly. Blockbuster had announced the policy as a permanent transformation. It reversed it — reinstating fees for some rentals — because the revenue impact was too large to sustain while also funding Blockbuster Online’s growth, managing the debt load from the 2004 Viacom spinoff, and maintaining the retail network.

The strategic response was not a solution to what Blockbuster had become. It was a bridge. When the bridge became too expensive to maintain, what remained was the same structural problem — a declining in-store rental business, a subscription competitor that had been accumulating advantages for five years, and a capital position that could not sustain both.

The Constraint Layer

Blockbuster Online faced five compounding disadvantages by 2005. They did not arrive in sequence. They shared the same resource pool.

The first was the distribution network gap. Netflix had been optimizing its network of distribution centers for one-day delivery since the late 1990s. By 2005, it operated more than forty facilities positioned to deliver to most of the U.S. subscriber base within a single business day. Blockbuster Online was building from zero in 2004. Matching Netflix’s delivery speed required years of network investment that would not generate returns until the network was built — investment funded from a balance sheet already weakened by the late-fee policy and the Viacom spinoff.

The second was the recommendation engine gap. Netflix launched its Cinematch recommendation algorithm in 2000. By 2006, the system had six years of behavioral data from millions of subscriber interactions. In October 2006, Netflix publicly announced the Netflix Prize — a $1 million competition to improve Cinematch’s accuracy by ten percent — a move that simultaneously drove product improvement and demonstrated the scale of the behavioral dataset to anyone paying attention. Blockbuster Online launched with a smaller subscriber base and a recommendation system with years less training data. The gap was not static. It widened with each additional month of Netflix operation.

The third was the catalog utilization structure. Netflix’s recommendation engine, by directing subscribers toward catalog titles, reduced the pressure on new-release inventory — historically the most expensive and competitive part of the rental model. Subscribers who regularly watched catalog titles needed fewer of the same new releases that every competitor was also trying to stock. This reduced costs while improving subscriber satisfaction. Blockbuster’s store-based model remained dependent on new-release traffic.

The fourth was the capital position. Blockbuster entered the critical competitive window — 2004 through 2006 — with debt from the Viacom spinoff, declining in-store revenues, the revenue cost of the No Late Fees policy, and escalating Blockbuster Online investment requirements. Netflix, by contrast, reached profitability in 2003 on a subscriber base of approximately 1.5 million — before Blockbuster Online launched — and was funding its growth from a clean balance sheet with steady recurring revenue. The capital asymmetry meant that every competitive move Blockbuster made cost more than the equivalent move by Netflix.

The fifth constraint was organizational. Blockbuster’s retail network — approximately nine thousand stores at its peak — was simultaneously its most valuable asset and its primary competitive disadvantage. The stores generated revenue, employed tens of thousands of people, supported a real estate and supply chain infrastructure, and defined the brand. They also generated the cost structure that made the revenue sacrifices required to compete with Netflix operationally unsustainable. Blockbuster could not become Netflix while remaining Blockbuster. Each constraint pulled from the same pool of capital and organizational attention that every other constraint also required.

The Compression

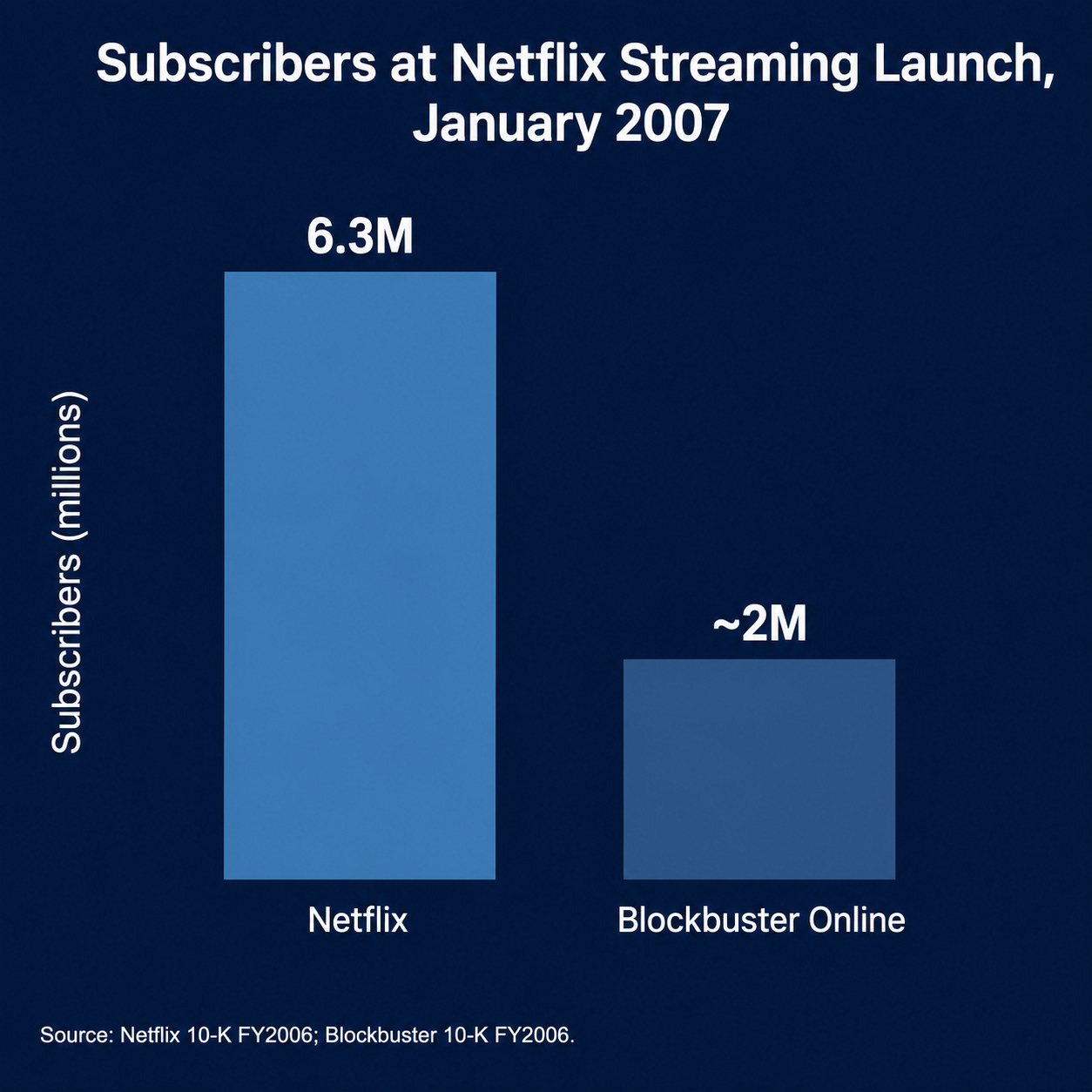

In January 2007, Netflix announced that it would offer streaming video as a feature for existing subscribers — at no additional charge — using the infrastructure already in place.

The streaming service launched not into an empty market but into an existing base of 6.3 million monthly subscribers, each with a credit card on file and a billing relationship with Netflix. The recommendation engine that would surface streaming titles had been trained on seven years of subscriber behavior. The brand identity associated with no-friction access to film had been built over eight years. The direct consumer relationship — unmediated by any physical location — had existed since the first subscription billing in 1999.

None of this was built for streaming. It was built to retain DVD subscribers. But the infrastructure requirements for a streaming launch — a direct billing relationship, a recommendation system, a brand identity around frictionless access, a subscriber base already paying monthly — were identical to the infrastructure Netflix had built for the DVD subscription model. The streaming transition was not a new beginning. It was a transfer.

Blockbuster entered bankruptcy in 2010, its capital exhausted and its strategic window closed. The DVD era was not the prelude to the interesting part. It was where the position was built.

What Netflix Left Behind

The standard framings of this story locate the decisive moment in different places — Reed Hastings’ foresight, Blockbuster’s complacency, the inevitability of the internet disrupting physical retail. Each of these frames carries some truth and misses the structural mechanism.

Hastings had foresight. But the decisions that built Netflix’s structural position were not primarily acts of foresight. The subscription model was an operational experiment. The no-late-fee policy was a customer retention mechanism. Cinematch was a solution to an inventory utilization problem. The distribution network was a response to subscriber complaints about delivery wait times. None of these were announced as moat-building. They became a moat because each one reinforced the others and because the model that made them necessary also made them valuable.

Blockbuster was not complacent. Blockbuster Online was a genuine, well-funded competitive response that reached one million subscribers in under a year. The problem was not effort — it was that the required response involved simultaneously dismantling a revenue model the company depended on, building capabilities from zero that Netflix had been building for five years, and sustaining losses on a balance sheet that could not absorb them indefinitely. That is not complacency. That is a structurally constrained position.

The internet did disrupt physical retail. But the streaming transition built on a foundation that had nothing to do with the internet. The subscriber relationship, the billing infrastructure, the recommendation engine, the brand identity — all of it came from eight years of DVD subscription operations.

The structural advantage Netflix carried into the streaming era was not technological. It was relational. It was the accumulated product of eight years of monthly billing, behavioral data collection, and retention-driven investment.

Discussion Question

Netflix’s structural advantages during the DVD era accumulated from decisions that were made for operational reasons — retention, cost management, inventory utilization — rather than as deliberate moat-building. The subscription model, the no-late-fee policy, the recommendation engine, the distribution network: each was a response to an immediate problem that happened to compound the others.

The question worth sitting with: if the structural advantage was not the product of deliberate strategy, what does that suggest about how durable advantages actually form — and how much of what we call strategic foresight is the retrospective framing of decisions that worked out?

If you have a view on this, I’d like to hear it. Leave a comment below.

The podcast version is available wherever you listen to podcasts or at deliberatedriftpodcast.com