Spirit Airlines: The Low-Cost Model Was Working

How a structurally efficient airline accumulated constraints it couldn't resolve when the environment shifted.

In 2014, Spirit Airlines was the most profitable airline in the United States.

Not the largest. Not the most admired. By almost every measure of the passenger experience, it ranked near the bottom of the industry. But on operating margin, it sat at the top — ahead of Delta, ahead of Southwest, ahead of every carrier that offered more legroom, more reliability, and a reason to come back.

The model that produced that result was not complicated. Strip the product to its functional minimum. Charge the lowest possible base fare. Then charge separately for everything else — the bag, the seat selection, the itinerary change. Keep the aircraft moving. Keep the costs below what any legacy carrier could match. The gap between what Spirit charged and what a legacy ticket cost was wide enough that no amount of discomfort closed it for a price-sensitive traveler.

That gap was the business. Not the planes, not the routes, not the brand. The gap.

Bill Franke, who served as Spirit’s chairman during its most profitable years, said in 2025 that the original ultra-low-cost carrier model — where an airline competes primarily on base fare by stripping the product to its functional minimum — was gone for good in the United States. He was describing what had already happened to the industry. He was also describing what had already happened to Spirit.

On May 2, 2026, Spirit Airlines ceased operations. It was the first significant U.S. carrier to shut down in twenty-five years. Seventeen thousand direct and indirect employees lost their jobs. Millions of passengers held tickets that were immediately worthless.

The coverage that followed reached for the most visible explanation. Jet fuel prices had surged following U.S. and Israeli strikes on Iran in February 2026. A government bailout had been negotiated and then collapsed when a key creditor group rejected the terms. The airline had filed for Chapter 11 bankruptcy protection twice in less than a year.

All of that is accurate. None of it is the structural story.

Spirit did not fail because a war sent fuel prices up. It failed because the condition its model required to function — a price gap wide enough to justify every tradeoff the product asked of its passengers — had been closing for a decade. By the time the fuel shock arrived, there was nothing left to absorb it.

The System

Spirit’s ultra-low-cost model worked through a logic that was internally consistent and, for a time, genuinely difficult to compete with.

The mechanism began with the base fare. By stripping out every included service — carry-on bags, seat selection, itinerary flexibility, snacks, printed boarding passes — Spirit could price its tickets at levels no legacy carrier could match without losing money on the route. In 2011, Spirit’s base fares ran roughly forty percent below the industry average. Even after a passenger paid every applicable fee, the total price was still around thirty-five percent lower than a comparable legacy ticket.

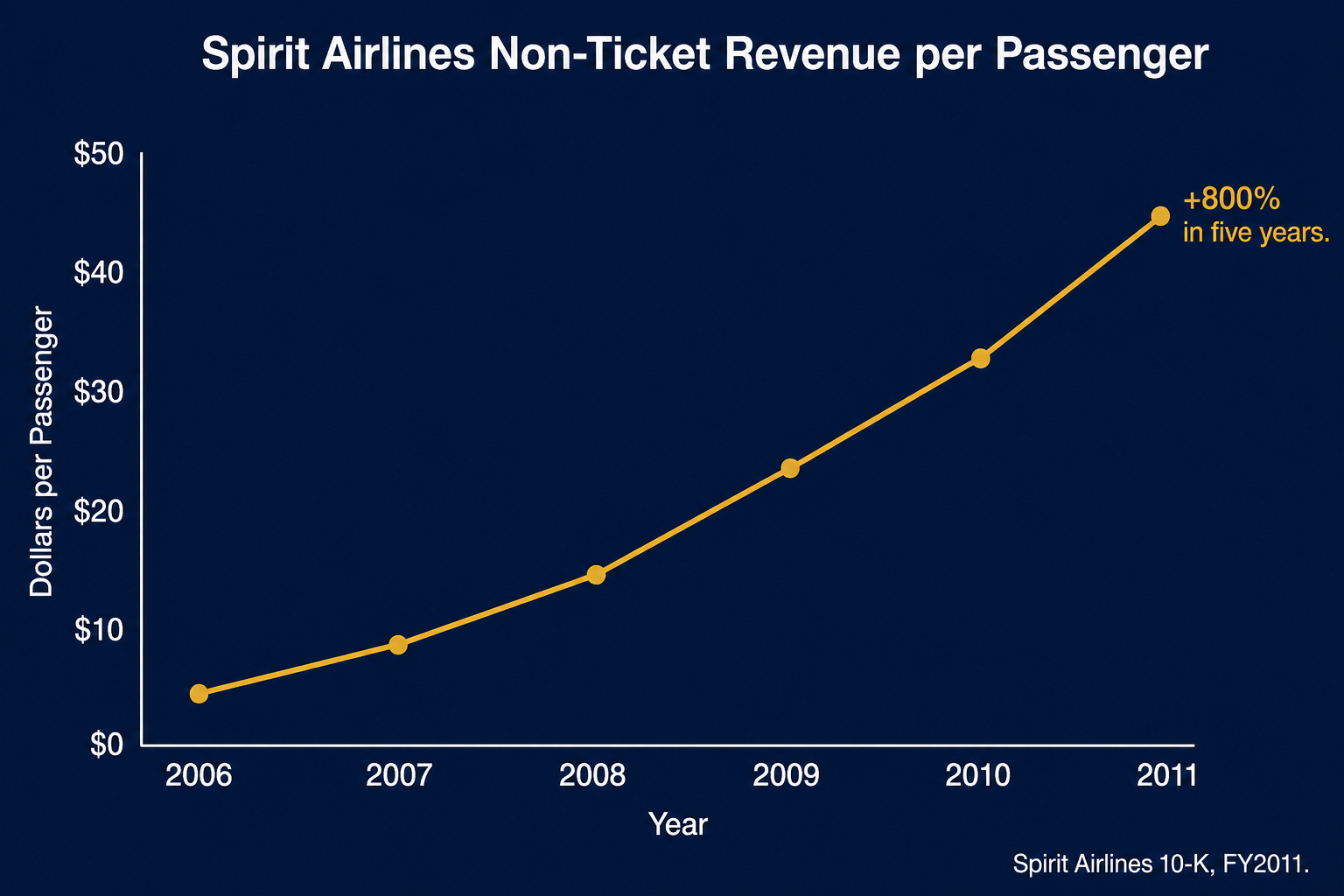

Those fees were not incidental to the model. They were load-bearing. Non-ticket revenue per passenger grew from around five dollars in 2006 to forty-five dollars by 2011 — an increase of roughly eight hundred percent in five years.

The fees funded the operation. They also shaped it. Charging for carry-on bags reduced the weight passengers brought onto aircraft, which reduced fuel consumption and shortened turn times at the gate. The fee structure was simultaneously a revenue mechanism and an operational discipline.

The result was a flywheel. Low fares filled seats. Full aircraft spread fixed costs across more passengers. Low unit costs allowed fares to stay low. The airline’s 2011 annual filing describes this logic explicitly — the model was designed so that each component reinforced the others.

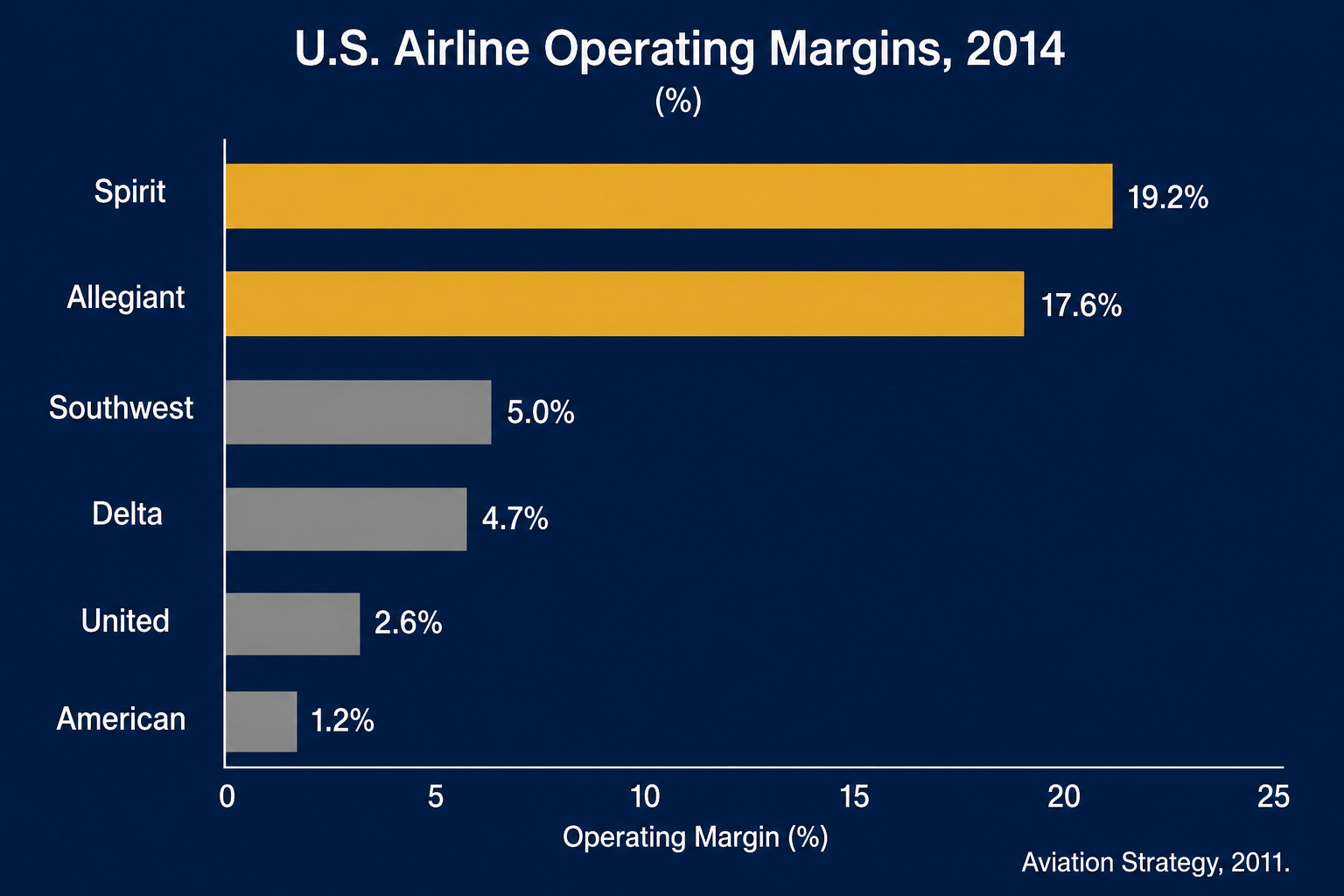

At peak, it worked. Spirit and Allegiant were the two most profitable U.S. airlines in 2014, at operating margins of 19.2 and 17.6 percent respectively. The legacy carriers — Delta, United, American — were profitable, but not at those margins. Spirit had built something the industry’s largest players could not replicate without dismantling their own cost structures.

The condition the model required was simple: the price gap had to be wide enough that passengers would accept the tradeoffs. No seat selection. No free bag. No flexibility. A Spirit ticket had to be cheap enough that the answer to every inconvenience was the price.

That condition held as long as legacy carriers couldn’t get close. It held until they could.

The Shift

Delta introduced basic economy fares in 2015. By early that year, the product was available in seventy-five markets, many of them overlapping directly with Spirit routes. United and American followed. The structure was familiar: non-refundable, no seat selection, bag fees required. The restrictions mirrored Spirit’s in almost every meaningful way.

What the legacy carriers kept was what Spirit had never had. Loyalty program miles. Hub network access. Operational reliability built on decades of infrastructure. A basic economy fare from Delta was not identical to a Spirit ticket — but it was close enough on price that the remaining differences started to matter.

Spirit’s chief executive Ben Baldanza acknowledged the pressure directly in December 2015, telling a Credit Suisse investor conference that Delta was very aggressive toward a carrier like Spirit and made it hard to grow in their markets. He argued the model was resilient enough to absorb it. He was not wrong that Spirit could absorb it. He was describing a ceiling, not a floor.

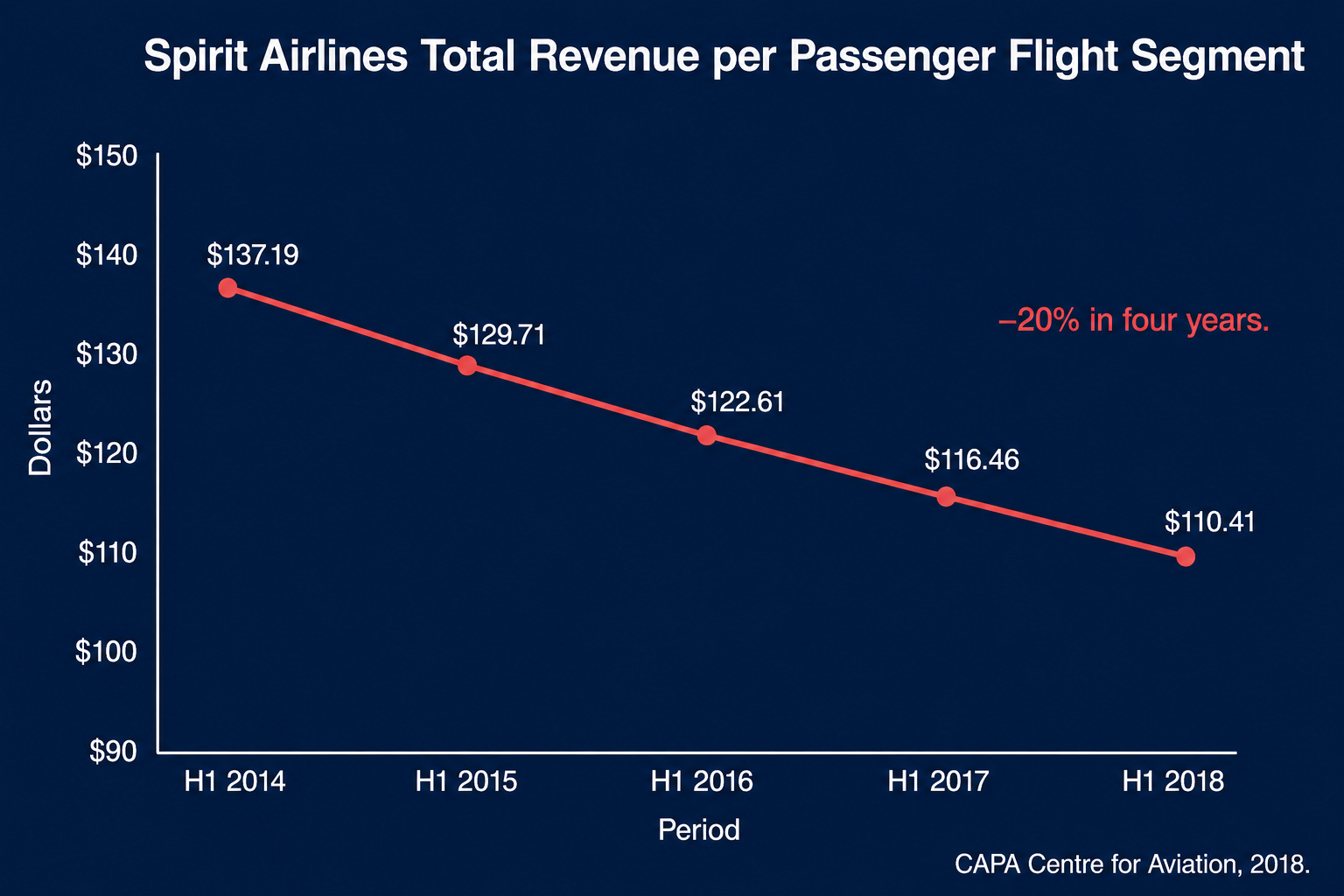

The numbers tracked the shift. Spirit’s total revenue per passenger flight segment fell from $137.19 in the first half of 2014 to $110.41 in the first half of 2018 — a decline of nearly twenty percent over four years. By 2018, Spirit’s own executives acknowledged in contemporaneous analysis that their price point was no longer always the lowest in the market.

The gap was closing. Not because Spirit’s costs were rising faster than expected — they were rising, but so were everyone else’s. The gap was closing because the legacy carriers had absorbed the lesson Spirit had taught the industry and applied it with resources Spirit could not match.

This is the shift the fuel shock coverage skipped. The external crisis in 2026 was real. But the structural condition that made Spirit vulnerable to any external crisis had been developing for a decade before a single Iranian facility was struck.

The Response

Spirit’s response to the competitive shift took two forms, and both were rational given what management could see at the time.

The operational response was to push harder on the levers the model provided. More routes. More aircraft. Higher utilization. The theory was straightforward: if the margin per passenger was compressing, volume could compensate. The airline grew its fleet aggressively through the late 2010s, reaching 194 aircraft by the end of 2022 — a thirty-four percent increase from its pre-pandemic size.

Ancillary revenue kept climbing in absolute terms, reaching $3.0 billion in 2023 against $1.1 billion in 2021. But the growth was masking the underlying problem. Non-ticket revenue per passenger was rising only marginally while fare revenue per segment was falling sharply. By the third quarter of 2023, total revenue per passenger flight segment had dropped 13.5 percent year over year, to $116.43. Fare revenue per segment was down 27.8 percent. The ancillary ceiling had been reached. There was no more room to push.

The strategic response was a merger. In February 2022, Spirit agreed to be acquired by Frontier Airlines. In July 2022, Spirit’s board switched to a higher offer from JetBlue — a $3.8 billion deal that would have created the fifth-largest U.S. carrier.

What makes this decision analytically significant is not the outcome. It is the process. Spirit’s own board, in a filing with the Securities and Exchange Commission in 2022, characterized the regulatory risk of the JetBlue deal in explicit terms. The board described the transaction as facing substantial regulatory hurdles and assessed it as not reasonably capable of being consummated given the anticipated Department of Justice opposition. The board approved it anyway.

This was not recklessness. The merger was the only structural path available. A carrier that couldn’t solve its cost gap problem organically, and couldn’t outgrow it through volume, needed scale it couldn’t generate alone. The JetBlue deal was a bridge — an attempt to transfer Spirit’s structural problem into a larger organization that might manage it differently. The board understood the regulatory risk and concluded it was worth taking because the alternative was to remain independent with a narrowing model and no structural resolution in sight.

On January 16, 2024, a federal judge blocked the merger. Spirit’s stock fell approximately forty-seven percent that day.

The bridge had been removed. What remained was the problem — unmodified, and now without a crossing.

The Constraint Layer

Five constraints were operating simultaneously by the time the merger failed. None was individually fatal. Together, they left no room.

The first was the revenue model. The price gap Spirit’s model required had narrowed to the point where it could no longer reliably justify the product’s limitations. Legacy basic economy had accomplished what no amount of Spirit efficiency could reverse — it had moved the competitive floor up to meet Spirit’s ceiling.

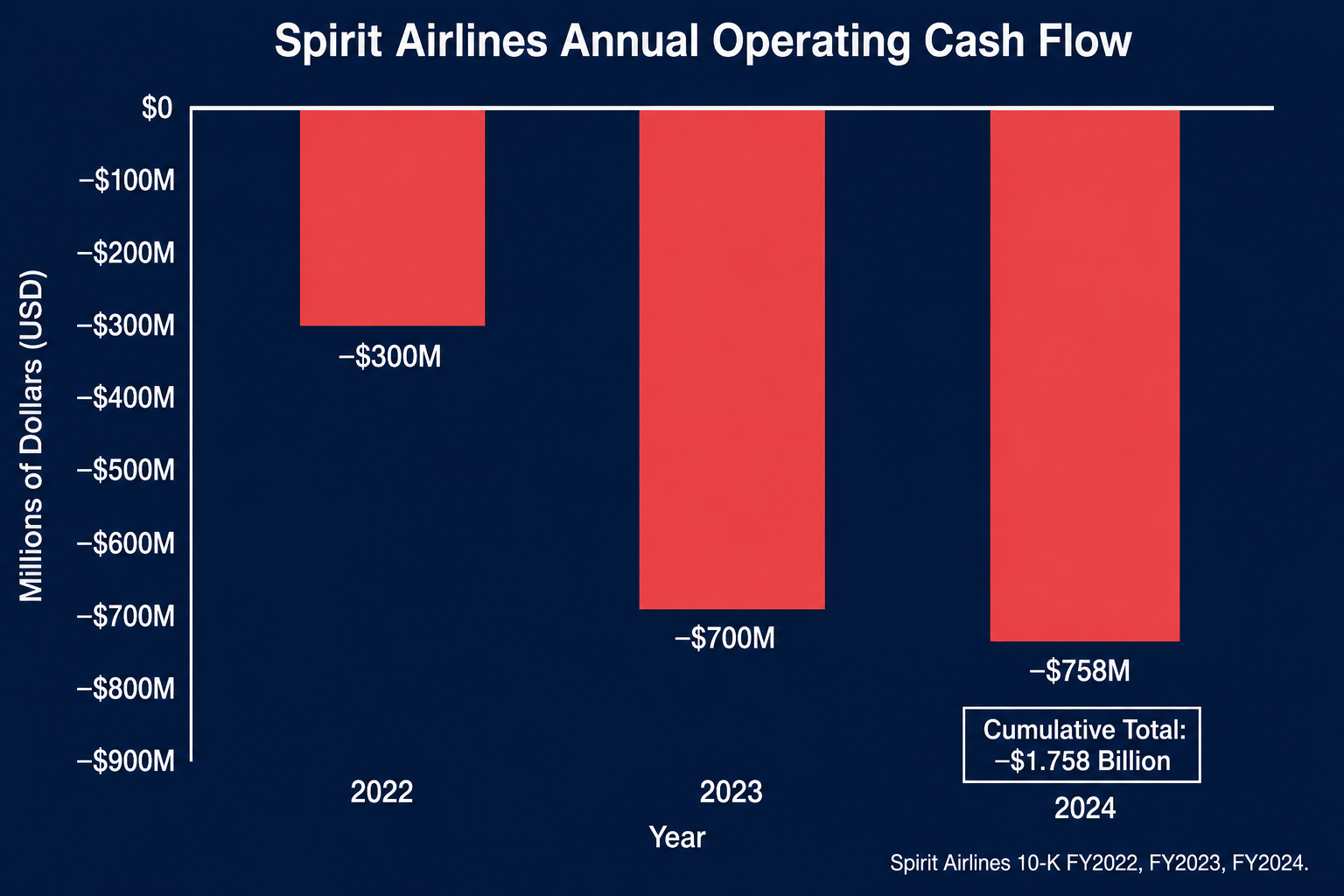

The second was the cost structure. Spirit’s unit costs had been among the lowest in the industry for years, and remained low in absolute terms. But the advantage was thinner than it had been. Labor costs rose from 22.1 percent of operating costs in 2022 to 28.1 percent in 2024. Operating cash flow ran negative $758 million in 2024. The cost discipline that had been the model’s foundation was holding — but the model it was holding up was no longer generating the returns that had once made the discipline worthwhile.

The third was the fleet. Spirit had taken delivery of new Airbus A320neo aircraft through the growth period, modernizing its operation. But when Pratt & Whitney issued a recall on geared turbofan, or GTF, engines in 2025, Spirit’s fleet was disproportionately affected. All seventy-nine of its GTF-powered aircraft required inspection and potential replacement. The recall process was expected to take more than two years. Planes on the ground don’t generate revenue, and Spirit had no reserve capacity to absorb the gap.

The fourth was capital. The airline ended 2022 with $1.8 billion in liquidity — a buffer that looked sufficient at the time. Three years of operating losses consumed it. The first bankruptcy filing, in November 2024, targeted a restructuring from $7.4 billion in total debt and lease commitments to $2.1 billion. The second filing, in August 2025, came before the restructuring had stabilized. By April 2026, Spirit’s attorney told the bankruptcy court that the airline’s cash was not going to last for very much longer.

The fifth was organizational identity. Spirit had built its entire operation — its cost structure, its customer base, its brand position, its internal culture — around the ultra-low-cost model. That identity was not a liability in the years when the model worked. It became one when the model stopped working, because it foreclosed the range of responses available. Spirit could not move upmarket without abandoning the cost discipline that kept it competitive. It could not build a loyalty program that competed with Delta’s without the network infrastructure Delta had spent decades constructing. It could not become something else, because everything it was had been built to be this one thing.

Five constraints. The same window. No reserves. No available exit.

The Compression

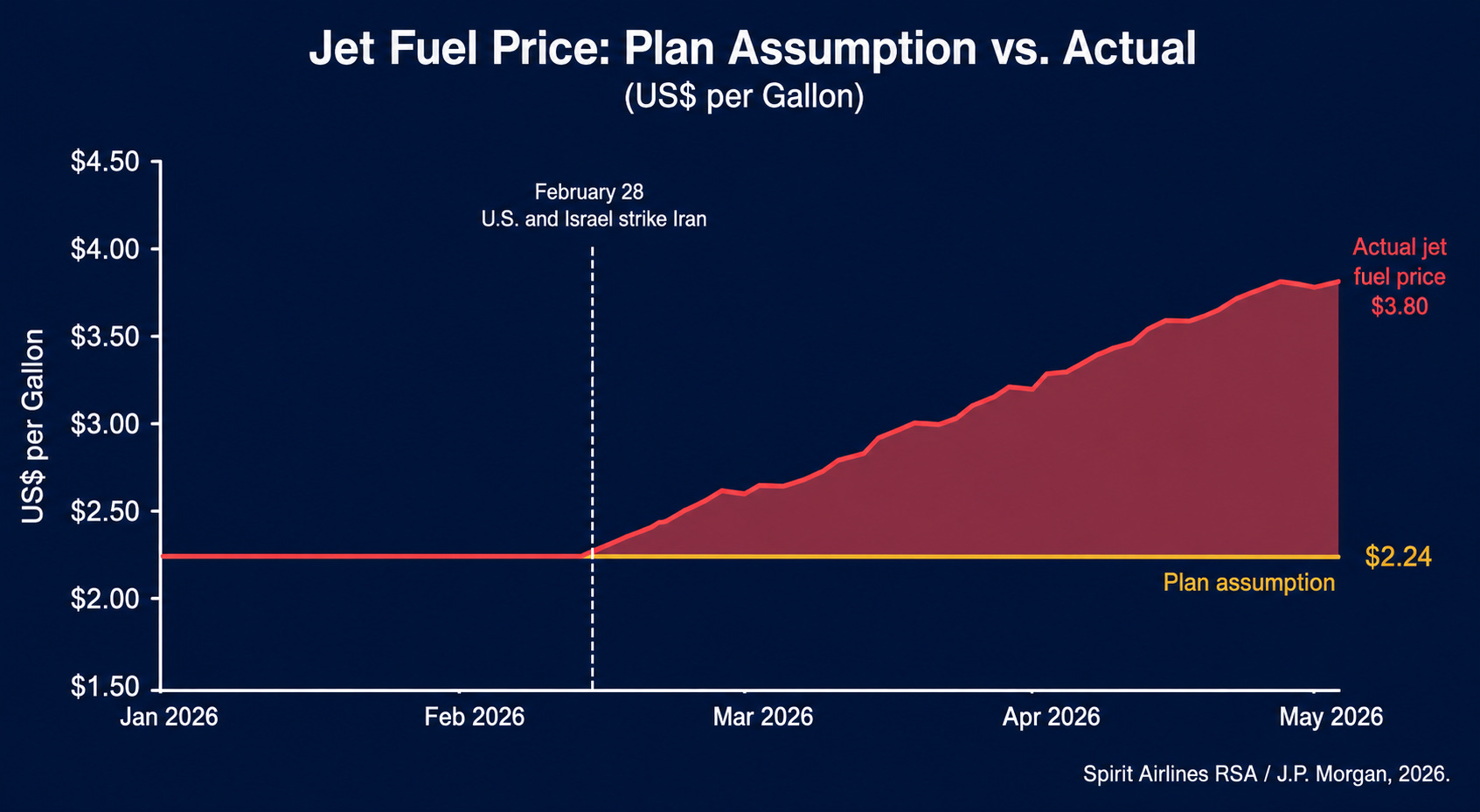

The restructuring plan Spirit filed in November 2024 was built on assumptions that were reasonable at the time. The airline projected a return to positive operating margins by the first quarter of 2026, moving from negative 27.1 percent in the first quarter of 2025 to negative 5.6 percent a year later. A net profit of $219 million was projected for 2027. The plan required fuel prices to remain stable, bookings to recover as the fleet stabilized, and creditor patience to hold while the restructuring took effect.

The fuel price assumption embedded in the restructuring support agreement was $2.24 per gallon for 2026.

On February 28, 2026, the United States and Israel conducted strikes on Iran. Jet fuel prices rose approximately seventy percent from that point. J.P. Morgan estimated that if fuel remained at $4.60 per gallon, Spirit’s projected 2026 operating margin would deteriorate from positive 0.5 percent to approximately negative twenty percent — adding roughly $360 million in costs the plan had not anticipated and the balance sheet could not absorb.

Spirit’s chief executive Dave Davis said in the wind-down statement that the sudden and sustained rise in fuel prices had left the airline with no alternative but to pursue an orderly wind-down. He was accurate. The fuel shock was the proximate cause of the closure.

But the restructuring plan had required all of its assumptions to hold simultaneously. Fuel stability. Booking recovery. Fleet availability. Creditor alignment. When one failed, the others became irrelevant. The plan was not designed to survive a shock of that magnitude because no plan calibrated to Spirit’s available resources could have been.

The fuel shock did not create Spirit’s problems. It revealed the degree to which every buffer had already been consumed.

Spirit ceased operations at 3:00 a.m. on May 2, 2026. The final flight landed at Dallas–Fort Worth shortly after midnight, arriving from Detroit.

The Ending

Three framings have dominated the coverage of Spirit’s closure, and all three are incomplete.

The first is that the Department of Justice killed Spirit by blocking the JetBlue merger. The merger’s failure was consequential — it removed the one structural path that might have resolved Spirit’s position. But the constraint accumulation that made a merger necessary had been building since 2015. A carrier whose model was structurally intact does not need a merger to survive. Spirit needed one because its model was already under pressure when the deal was announced.

The second is that the Iran war killed Spirit. The fuel shock was real, and at the margin it was decisive — it invalidated the one assumption the restructuring plan could not survive losing. But Spirit had filed for bankruptcy twice before a single Iranian facility was struck. The war accelerated a conclusion the financials were already approaching.

The third is that Spirit was simply a bad airline that deserved to fail. This framing mistakes the product for the business. Spirit was not beloved. It ranked second-worst among the ten largest U.S. carriers for passenger complaints in both 2023 and 2024. But its presence in a market suppressed fares by approximately fourteen percent on routes it served. Some routes were projected to see fare increases of fifteen to twenty percent following its closure. You did not have to fly Spirit to benefit from Spirit flying.

What the structural story reveals is something the simpler framings don’t reach. Spirit’s model worked because it created a price gap the industry couldn’t close. The industry closed it anyway, not by matching Spirit’s costs, but by matching its price points with a product that retained advantages Spirit had never built and couldn’t build. The model didn’t fail because Spirit stopped executing it. It failed because the competitive environment stopped rewarding it.

U.S. Transportation Secretary Sean Duffy said on the day of the closure that Spirit was in dire straits long before the war with Iran. He was describing the outcome. The structural story is about why the straits narrowed — and how long it took for the narrowing to become visible to everyone who hadn’t been watching the gap.

Discussion Question

The Department of Justice blocked Spirit’s merger with JetBlue in January 2024 on the grounds that eliminating Spirit as an independent competitor would harm consumers. Eighteen months later, Spirit filed for bankruptcy for the second time. Sixteen months after that, it ceased operations entirely — taking its fare-suppressing effect with it.

When a regulator intervenes to preserve competition, it is making a prediction about what the market will look like with and without the intervention. The DOJ predicted that a JetBlue-Spirit merger would reduce competition and raise fares. It may have been right about the merger. It does not appear to have been right about the alternative.

If regulators can model the competitive risks of consolidation but struggle to model the structural trajectory of the companies they’re protecting, what should the standard for intervention actually be?

If you have a view on this, I’d like to hear it. Leave a comment below.

The podcast version is available wherever you listen to podcasts or at deliberatedriftpodcast.com.