Fisker: The Asset-Light Strategy Made Sense

How a clean-sheet EV company built a model that required conditions it couldn't control.

Henrik Fisker had watched one car company carry his name into bankruptcy already. The first Fisker Automotive collapsed in 2013, taking its federal loan and its half-finished factory with it. When he started again in 2016, he built the second company around a different idea: the factory was the problem. He wasn’t going to build one.

Instead, he struck a deal with Magna International, one of the largest automotive suppliers in the world. Magna’s contract manufacturing division, Magna Steyr, operated a plant in Graz, Austria, that already built the Jaguar I-Pace — a battery electric vehicle, at scale, for a premium brand. The arrangement was straightforward: Magna would manufacture the Fisker Ocean to Fisker’s specifications, and Fisker would pay per vehicle produced. No factory. No billion-dollar construction timeline. No manufacturing hell.

In October 2020, Fisker merged with a publicly listed shell company — a structure called a special purpose acquisition company, or SPAC, which lets a private business go public quickly without the usual stock market listing process — and arrived on the NYSE with roughly one billion dollars. The model looked smart. The partner was credible. The vehicle, a premium electric SUV called the Ocean, had generated real consumer interest.

Fisker filed for bankruptcy in June 2024.

When it did, the Magna production line had been idle for four months. Talks with a large established automaker about a potential rescue had collapsed. Cash was nearly gone. The company had no factory, no alternative way to build its vehicle, and no path back to revenue.

The story that followed Fisker into bankruptcy court was about money: not enough of it, spent too fast, in a market that had cooled on electric vehicles. That story is true as far as it goes. But it doesn’t go far enough. The money ran out because the business model consumed it without generating enough revenue to sustain itself. And the business model was built that way from the start. The problem wasn’t the market, or the timing, or the capital raise. The problem was a single dependency — on Magna’s willingness to keep producing — that nothing in the original deal required Magna to maintain when Fisker ran short of cash.

The System

To understand why Fisker chose the path it did, you have to understand what the alternative looked like in 2020.

Tesla had nearly died building its Fremont factory. The company came within weeks of bankruptcy during the Model 3 production ramp in 2018 — Elon Musk was sleeping on the factory floor trying to solve assembly line problems by hand. Rivian, which had raised billions before delivering its first truck, was burning through capital so fast that analysts questioned whether it would survive long enough to reach meaningful sales volume. The pattern was consistent enough to have a name: manufacturing hell. Every electric vehicle startup that tried to build its own factory discovered that automotive manufacturing was extraordinarily difficult, extraordinarily expensive, and extraordinarily unforgiving of the mistakes that new companies inevitably make.

Fisker’s answer was to skip the factory entirely. Outsource manufacturing to a company that already knew how to do it. Keep Fisker focused on design, software, and brand — the things that create the experience a customer pays for — and pay Magna to handle everything else. This model is sometimes called asset-light, meaning the company avoids owning the heavy, expensive physical assets — the factories and machinery — that traditional manufacturers carry on their books.

Magna Steyr was not a speculative choice. It had built the I-Pace at Graz. It had built the Mercedes-Benz G-Class. It had built the BMW Z4. These were complex, premium vehicles with demanding customers and zero tolerance for quality failures. Magna knew how to build cars. Fisker wasn’t asking it to learn.

The Ocean came in four versions — the Sport at around thirty-seven thousand dollars, the Ultra and Extreme in the middle, and a limited One edition at the top — giving Fisker a range of price points without building separate platforms. Reservations came in. The thesis seemed to be holding.

There was one thing the model required to function. Magna had to keep producing. Everything else — the revenue, the brand, the survival of the company — depended on that single relationship staying intact.

Magna’s financial stake in Fisker’s success amounted to options to buy about 19.4 million Fisker shares at a penny each. It was not a partnership in any meaningful sense. Magna built vehicles. Fisker paid per vehicle. When Fisker couldn’t pay, Magna had no financial reason to keep building.

The Shift

Production began at Graz in late 2022. First deliveries went to European customers before the year ended. American deliveries started in mid-2023.

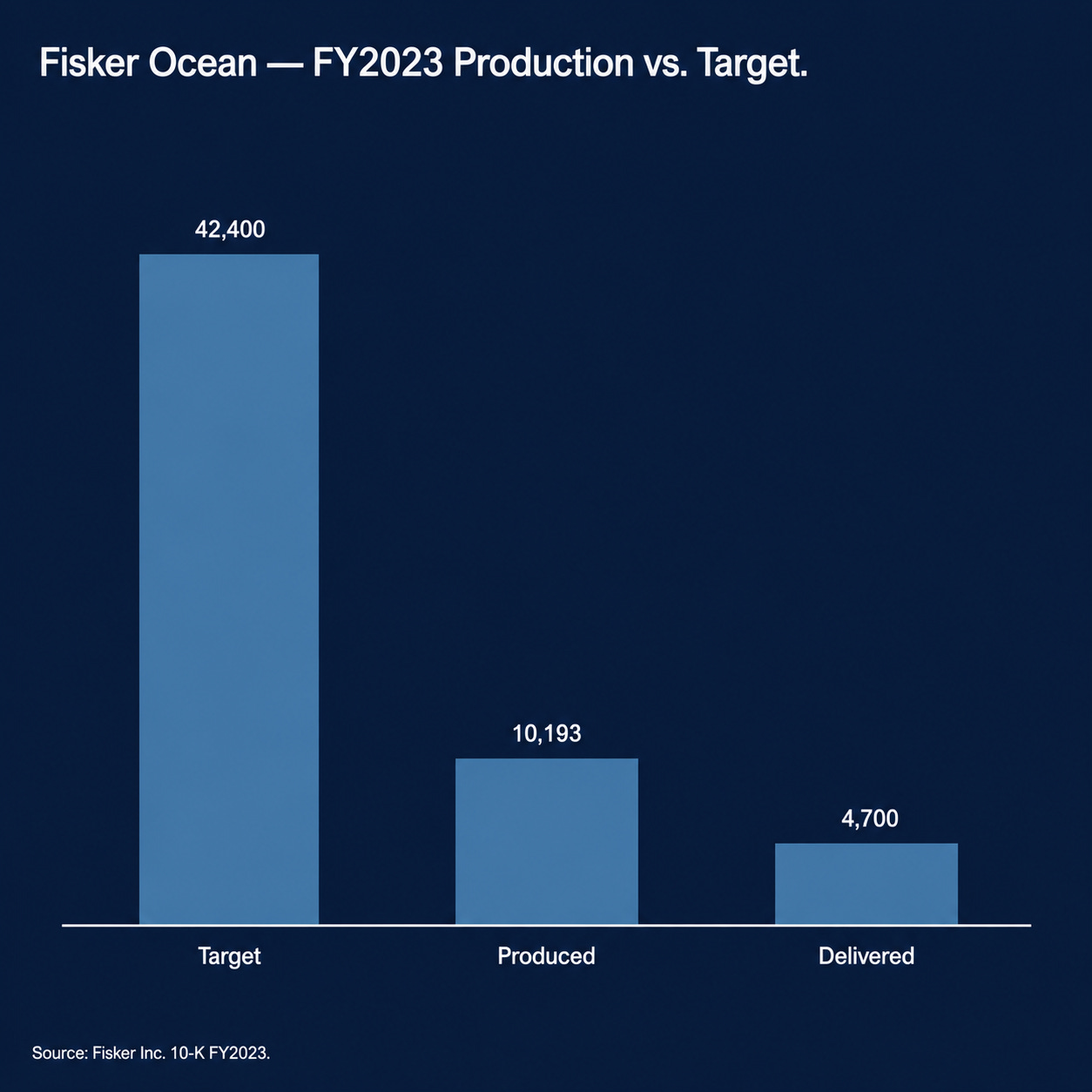

Fisker had planned to produce around 42,400 vehicles in 2023. It produced around 10,000. Deliveries fell short of even that number. By the end of the year, thousands of finished Oceans were sitting in storage — built, paid for, and unsold.

The Ocean had problems. The federal agency responsible for vehicle safety, the National Highway Traffic Safety Administration (NHTSA), opened investigations. Fisker issued multiple recalls covering door latches, brakes, and software. Reviews from automotive journalists were mixed in a specific and damaging way: the design was praised, the driving experience was often praised, but the software was unreliable and the build quality was inconsistent. That combination — a vehicle that felt promising but didn’t feel finished — is harder to recover from than a vehicle that is simply bad. A bad vehicle gives you a clear problem to solve. A half-finished one gives you a story that travels.

Each recall cost money. Each vehicle sitting in a storage lot was money already spent on production that hadn’t come back yet. The gap between when Fisker paid Magna to build a car and when a customer actually took delivery was the gap the company was slowly drowning in. Fisker paid per vehicle produced. Revenue only arrived when a vehicle was delivered. The wider that gap got, the worse the cash position became.

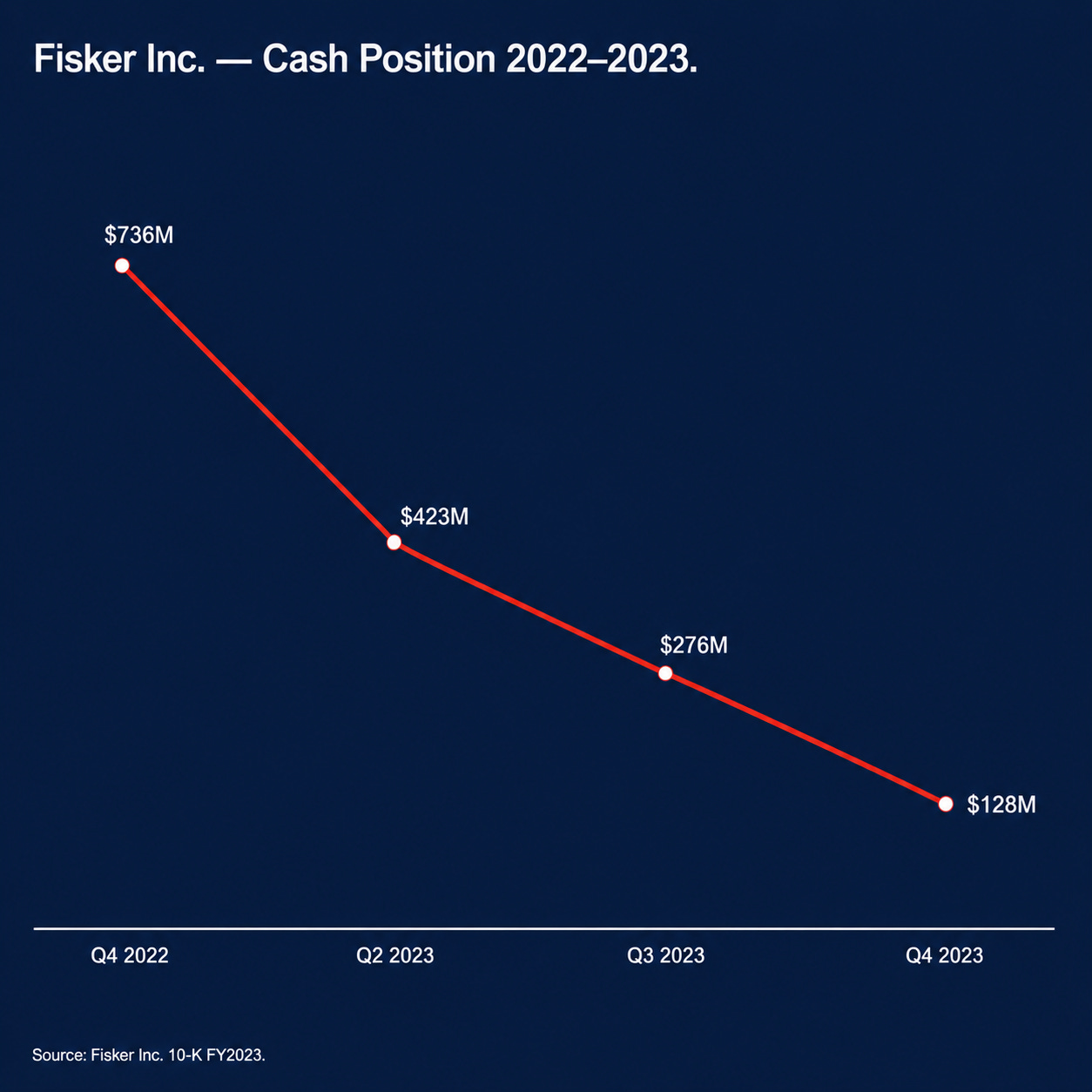

By the end of 2023, Fisker’s auditors had seen enough. The annual financial filing disclosed what the auditors had formally concluded: there was substantial doubt about whether the company could survive the next twelve months. This is a specific accounting term — a going concern warning — that auditors are required to issue when the numbers raise serious questions about a company’s ability to keep operating. Cash on hand was about 128 million dollars. At the rate Fisker was spending, that was months, not years.

Magna was watching all of this. It could read the same filing. And it had its own clients — Mercedes, BMW, Jaguar — whose vehicles shared the Graz facility with the Ocean. When the question shifted from ‘will Fisker pay us’ to ‘can Fisker pay us,’ the calculation changed.

The Response

Fisker tried two things.

The first was to cut prices. Discounts on the Ocean started appearing in late 2023, designed to move the vehicles piling up in storage and get cash coming back in. It worked, to a point. Vehicles moved. Cash came in. But discounting a car that was supposed to represent premium value sends a signal to the market that is very hard to unsend. Every buyer who paid full price is now looking at a cheaper version of what they bought. Every prospective buyer now knows the price is negotiable. Dealers watch residual values — what the car will be worth when customers trade it in — and those were falling. The discount strategy solved a short-term cash problem while making the long-term brand problem harder.

The second move was to find a buyer. By late 2023, Fisker’s leadership understood clearly that the company could not survive independently. What it needed was a large, established automaker — the kind of company, sometimes called an original equipment manufacturer or OEM, that has its own factories, its own supply chains, and a balance sheet that doesn’t depend on a single vehicle selling well in its first year. Talks began. Reuters reported in early 2024 that Nissan was involved. Fisker confirmed in a regulatory filing on March 22, 2024 that discussions with a large automaker had taken place and had ended without a deal.

Neither move addressed the actual problem. The discounts helped with cash but didn’t fix the Magna relationship, the recall backlog, or the production ramp. The acquisition talks, if they had succeeded, might have addressed all of it — but by the time those talks were happening, every number in Fisker’s public filings was visible to any prospective buyer. A going concern warning. A falling cash balance. Thousands of discounted vehicles in storage. A manufacturing partner that had already started asking when it was going to get paid. That is not a company anyone acquires on generous terms.

The acquisition talks were not a solution. They were a bridge. And by the time Fisker needed to cross it, the other side had already assessed what crossing would cost them.

The Constraint Layer

Five problems were running simultaneously through 2023 and into 2024. Each one made the others harder to solve.

The manufacturing dependency was the foundation of all of them. Fisker had no factory, no tooling, no way to build its own vehicles. It had chosen that deliberately. But it meant that every dollar of revenue the company would ever earn required Magna to keep producing. There was no backup. There was no partial solution. If Magna stopped, Fisker stopped.

The storage trap was the manufacturing dependency’s immediate consequence. Fisker had paid for thousands of vehicles that customers hadn’t taken yet. That money was gone — sitting in parking lots in the form of unsold cars. Moving those cars through discounts recovered some of it, but the discounts made the brand problem worse, which made it harder to sell future vehicles at the prices the business needed to survive. You couldn’t fix the cash problem without damaging the brand, and you couldn’t fix the brand without letting the cash problem get worse.

The recalls and quality issues added a third layer. Every recall meant engineering resources diverted to fixing problems on vehicles already delivered, at a moment when those same resources were needed to improve the software on vehicles still being produced. Every NHTSA investigation gave journalists and potential buyers another reason to hesitate. A reservation is only worth something when it converts to a sale. Fisker’s reservation list was not converting at the rate the business required.

The going concern warning changed the terms of every conversation Fisker was having. When a company’s auditors formally declare that its survival is in doubt, that declaration becomes public. Suppliers read it. Potential partners read it. Potential acquirers read it. Magna read it. Everyone who might have helped Fisker now had a documented reason to be cautious about how much exposure they were willing to take. The warning didn’t just reflect the company’s weakness — it deepened it.

And then there was identity. Fisker had been sold to investors, to customers, and to the market on a specific idea: that the asset-light model was smarter than building a factory. Henrik Fisker had built his public presence around that argument. To say out loud, in 2023, that the model wasn’t working would have been to repudiate the entire premise of the company at the moment the company most needed people to believe in it. So the story held. The discounts were framed as making the Ocean accessible. The production shortfalls were framed as temporary. The organizational identity had become a constraint on the honesty that might have opened different options.

Five problems. The same shrinking window. No reserves left to buy time with. No exit that didn’t require solving at least two of them simultaneously with money that was already running out.

The Compression

In February 2024, Magna stopped building the Ocean. Fisker hadn’t been paying its bills.

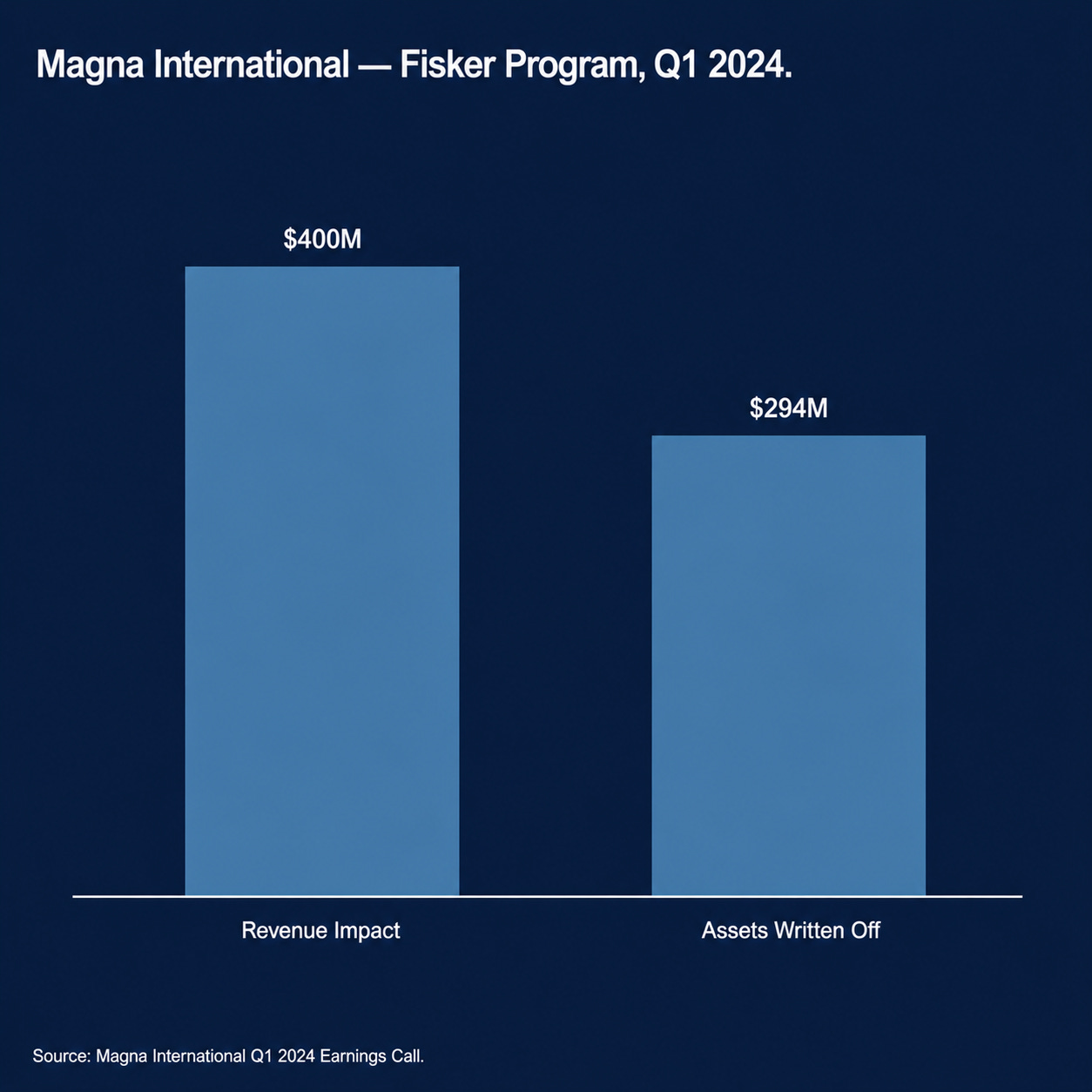

Magna’s chief executive Swamy Kotagiri addressed it directly on the company’s earnings call in May 2024. Production was idled. Their financial outlook assumed no further Ocean production. That assumption alone reduced Magna’s expected 2024 revenue by about 400 million dollars. In the same quarter, Magna wrote off its entire Fisker-related investment — the equipment at Graz allocated to Ocean production, and the share options it held — totaling 294 million dollars. Writing off an asset means concluding that it has no value left to recover. Magna had concluded the relationship was over.

The moment Magna stopped, Fisker’s revenue went to zero. Not reduced. Zero. There was no other product, no service income, no subscription revenue that could sustain the company while it figured out what to do next. The asset-light model had concentrated all of Fisker’s revenue into a single source — selling the Ocean — and that source required Magna. Without Magna, there was nothing.

On March 22, 2024, Fisker filed a regulatory disclosure confirming that the acquisition talks had ended. The company said it was exploring options: more financing, selling assets, restructuring its debts. These are the things a company says when it has run out of better options.

The moment the compression became irreversible wasn’t February 2024, when Magna stopped, or March 2024, when the acquisition talks collapsed. It was sometime in 2023, when Fisker’s cash burn rate and its deteriorating balance sheet crossed a threshold: the point at which any potential partner or acquirer could look at the numbers and conclude that a rescue would cost more than the company was worth. Everything after that threshold was consequence.

Fisker Inc. filed for bankruptcy on June 17, 2024, in the District of Delaware. The court process included an attempt to sell the business as a going concern — to find a buyer willing to keep it running rather than simply break it apart. No buyer came forward. The case converted to a full liquidation. The vehicles were sold. The company was wound down. The second company Henrik Fisker had built to carry his name was gone.

What Fisker Left Behind

Three explanations for what happened to Fisker circulate in the coverage. Each one is partially right. None of them gets to the actual problem.

The first is that Fisker ran out of money. This is true, but it skips the important question, which is why. Fisker raised nearly a billion dollars in its public listing and kept raising through 2021 and 2022. The capital was real. It ran out because the model consumed it without producing enough revenue to sustain itself — and the model was structured that way from the beginning. More money would have bought more time. It wouldn’t have changed the structure.

The second explanation is that Fisker got caught in the broader slowdown in electric vehicle demand. That slowdown was real, and it made everything harder. But Fisker’s structural problem existed independently of market conditions. A company with a single manufacturing partner and no leverage over that partner is vulnerable to the same dependency in a strong market — it just has more time before the vulnerability becomes visible. The market slowdown shortened the window. The window was already closing.

The third explanation is that the asset-light model failed. This is the closest, but it needs precision. The asset-light model as Fisker built it — with a single manufacturing partner, paid per vehicle, holding no meaningful stake in Fisker’s survival — created a dependency that contract terms alone couldn’t protect against. Magna was the right partner in 2020. The deal structure was not right for the risk Fisker was taking on. Those are different problems, and conflating them makes the lesson harder to see.

What Fisker actually demonstrated is something specific: that outsourcing manufacturing only works when the manufacturer has a genuine reason to absorb the difficulties that early-stage production always creates. A joint venture, a co-investment, a deal where Magna owned a real stake in Fisker’s outcome — any of those would have changed the incentives when payments started coming in late. A fee-for-service contract with a small share option attached did not.

The Fisker Ocean was a real car. It drove. People who drove it often liked it. The design was distinctive enough to attract buyers who weren’t just looking for a Tesla alternative. The company wasn’t a fraud. It was a genuine attempt to solve a genuine problem — how do you build an electric vehicle company without manufacturing hell — that ran directly into the limit of what the structure it chose could support.

The dependency was there from the start. It just took four years to matter.

Discussion Question

By late 2023, Fisker’s leadership could see clearly what was happening: the production shortfall, the vehicles piling up unsold, the cash running out, the auditor’s formal warning. They pursued the one option that might have saved the company — a deal with a larger automaker. What they couldn’t change was the position they were negotiating from. The balance sheet was public. The dependency on Magna was visible. The going concern warning was in the filing. The window for a deal on terms that would have preserved the company had already closed before the talks began.

Is asset-light manufacturing — outsourcing production rather than building a factory — a viable model for an early-stage vehicle company? Or does it only work when the manufacturer has a real financial stake in the outcome? And if Fisker had structured the Magna deal differently from the start — shared ownership, a joint venture, genuine skin in the game on both sides — would it have changed what happened in 2024?

If you have a view on this, I'd like to hear it. Leave a comment below.

The podcast version is available wherever you listen to podcasts or at deliberatedriftpodcast.com