Domino's: The Recipe Change Was Not the Story

How a pizza company spent a decade building delivery infrastructure competitors couldn't easily copy.

In late 2009, Domino’s Pizza did something unusual. The company ran a national advertising campaign built around footage of its own executives reading customer complaints aloud. The pizza, customers said, tasted like cardboard. The sauce tasted like ketchup. The crust tasted like nothing. Domino’s did not dispute this. It apologized, announced a complete reformulation of its core product, and invited the country to watch.

The campaign worked. First-quarter same-store sales in 2010 increased 14.3% — the largest quarterly jump in the company’s history at the time. Business press covered it as one of the more remarkable brand turnarounds in recent memory. The story was clean and legible: admit failure, fix the product, rebuild trust, recover.

The recipe change was necessary. Without it, Domino’s would have continued losing ground in consumer perception to Pizza Hut and Papa John’s, and the digital platform it was simultaneously building would have been selling a product nobody wanted. The recipe mattered. But it was not the structural event.

The structural event was a decade of capital allocation decisions — beginning around the same time as the recipe change and continuing through 2018 — that built proprietary delivery infrastructure, a digital ordering platform, and a franchisee economics model optimized around owned last-mile delivery. Those decisions looked like operational overhead while they were being made. Some looked like marketing gimmicks. One — the refusal to partner with third-party delivery platforms at the moment every other restaurant chain was signing with them — looked like stubbornness or overconfidence.

By the time the delivery economy arrived at scale, Domino’s had been building for it for a decade. The gap between Domino’s and its competitors was not a product gap. It was not a brand gap. It was an infrastructure gap that required rebuilding supply chain, technology, data, and franchisee economics simultaneously to close — and no competitor has closed it.

What follows is not the turnaround story. It is the story beneath it.

The System

Domino’s was founded in 1960 by Tom Monaghan in Ypsilanti, Michigan, on a simple and durable premise: pizza delivered fast to your door. The 30-minute guarantee — introduced in the 1970s and discontinued in 1993 following liability litigation — became the brand’s identity for three decades. Domino’s was not trying to make the best pizza. It was trying to make a reliable pizza arrive quickly.

That distinction matters for understanding what the company actually built during its growth period. The operational infrastructure required to fulfill a 30-minute delivery guarantee — driver networks, kitchen throughput systems, routing optimization, delivery radius management — was not incidental to the brand. It was the brand. When the guarantee was discontinued, the infrastructure remained. Domino’s entered the 2000s as the largest pizza delivery company in the United States by store count, carrying a delivery system that had been refined over thirty years and a product that consumer surveys consistently ranked below its primary competitors.

The business model was straightforward. Domino’s charged royalties to franchisees — ongoing percentage-of-sales fees for use of the brand — and generated additional revenue by selling food, equipment, and supplies to franchisees through an internal supply chain it owned and operated. Dough was manufactured in Domino’s facilities and distributed by Domino’s trucks to franchise locations. The company did not merely collect fees on system sales; it had a direct financial stake in franchisee volume through supply chain revenues that grew as system throughput grew.

This structure created a specific incentive: Domino’s had more to gain from increasing the number of orders flowing through the system than from extracting margin on individual transactions. That incentive would govern capital allocation decisions for the next two decades.

In 2004, Domino’s completed its initial public offering under Bain Capital ownership. The company carried significant long-term debt from its leveraged buyout structure — a capital constraint that would, in practice, concentrate spending on the highest-return infrastructure rather than dispersing it across brand extension or product premiumization.

Patrick Doyle joined the company in 1997, became President of Domino’s US operations in 2008, and was named chief executive in 2011. The decisions that produced the structural advantage were made primarily under his leadership.

The condition the system required to function was simple: customers needed to believe that Domino’s was a reasonable option for delivery. In 2008, that belief was eroding.

The Shift

Two structural shifts were underway simultaneously in the late 2000s, and Domino’s was positioned to respond to both — though the response to neither was immediately legible from outside the company.

The first shift was the rise of digital commerce as a primary ordering interface. By the late 2000s, the question of where and how a customer ordered was becoming as commercially significant as what they ordered. E-commerce had already restructured retail, travel, and media; the restaurant category was moving later and more slowly, but the direction was not ambiguous.

The second shift was slower and would not become fully visible until 2015 to 2018: the emergence of third-party delivery platforms. UberEats, DoorDash, and Grubhub began their aggressive US market expansion in that window, offering restaurants a distribution channel for delivery without the capital investment of building an owned delivery system. For most restaurant chains — built around dine-in or counter-service models with no existing delivery infrastructure — this looked like an opportunity. For a company that had spent decades building owned delivery infrastructure, it looked like a threat dressed as a partnership.

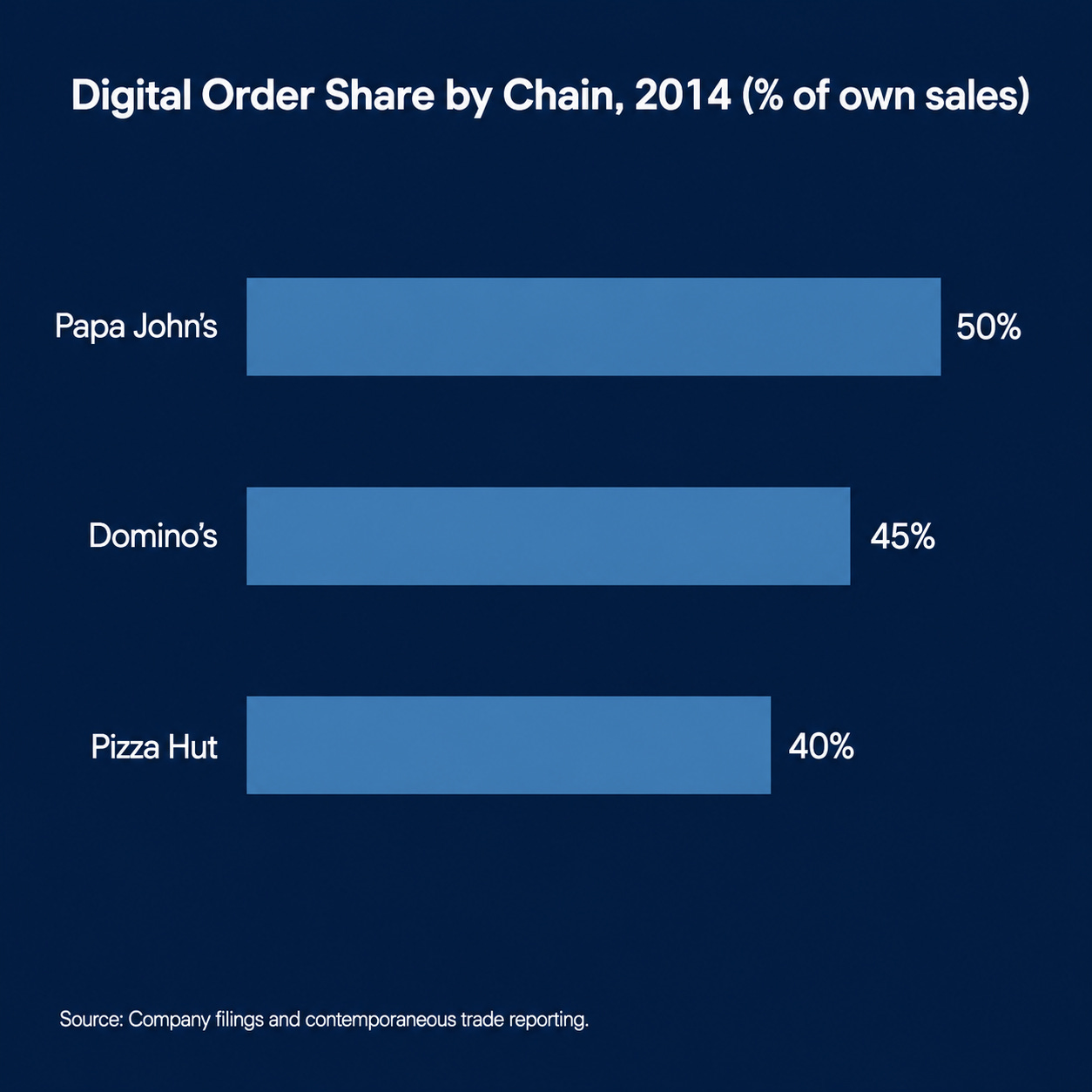

In 2014, the three major pizza chains were running close together on digital order share — each measured as a proportion of their own total sales. Papa John’s was the first to cross 50%, reaching that threshold in late 2014, while Domino’s was at approximately 45% and Pizza Hut at approximately 40%. The metric alone did not separate them. What separated them was what each company concluded the metric meant, and what each company decided to do about the second shift as it arrived.

By February 2018, that divergence was visible in a single transaction. Yum Brands — Pizza Hut’s parent company — entered a master services agreement with Grubhub and invested $200 million in Grubhub stock. Pizza Hut would use Grubhub’s platform, logistics, and last-mile delivery infrastructure for its US delivery channel. The decision was rational given Pizza Hut’s position: it had not built owned delivery infrastructure, and Grubhub offered a path to delivery volume without the capital cost of building it. Domino’s, which had been building that infrastructure for eight years, declined to partner with any third-party delivery platform during the same period. The two largest pizza companies in the world, at roughly similar digital order shares four years earlier, had arrived at structurally opposite positions on who would own the last-mile delivery relationship.

In late 2009, Christopher McGlothlin, then Domino’s chief information officer, announced that the company was pulling its technology development in-house. At the time, Domino’s had an internal technology staff of approximately 150. McGlothlin was direct about the reasoning: the company had concluded that the technology was too important to continue outsourcing. He was not describing a digital transformation initiative. He was describing a decision about where competitive advantage would be located.

That decision — made at the same moment as the recipe reformulation, and receiving almost none of the same coverage — was the structural inflection point.

The Response

What Domino’s did between 2010 and 2018 looked, from the outside, like a sequence of mostly unremarkable operational decisions interrupted occasionally by marketing novelties.

The digital ordering platform launched in 2010 and was built and maintained internally. The engineering team grew from the approximately 150 at insourcing to a dedicated technology facility — the Innovation Garage, opened in August 2015 — housing 150 technology team members in a 33,000 square foot building designed specifically for developing and testing ordering and logistics technology. By 2016, Patrick Doyle was describing Domino’s publicly as “a technology company that sells pizza.” This was not a rebranding exercise. It changed what the company hired for, what it invested in, and how it evaluated competitive threats.

The Domino’s Anyware program, developed from 2012 through 2015, extended the ordering interface across more than fifteen platforms: Twitter, text message, smart television, smartwatch, Ford Sync, Amazon Echo, Google Home, and others. Each integration was built and maintained internally. In the trade press, these launches were covered primarily as novelties — ordering pizza by tweeting a pizza emoji generated considerable coverage and considerable skepticism about whether anyone would actually use it. The coverage was not wrong about the novelty. It missed the accumulation. Each integration was adding ordering surface area and, behind it, data. By 2014, Domino’s had launched Pizza Tracker — real-time order tracking with named driver identification and stage-by-stage updates. It was the first of its kind in the restaurant industry. It looked like a customer experience feature. It was also a logistics management system.

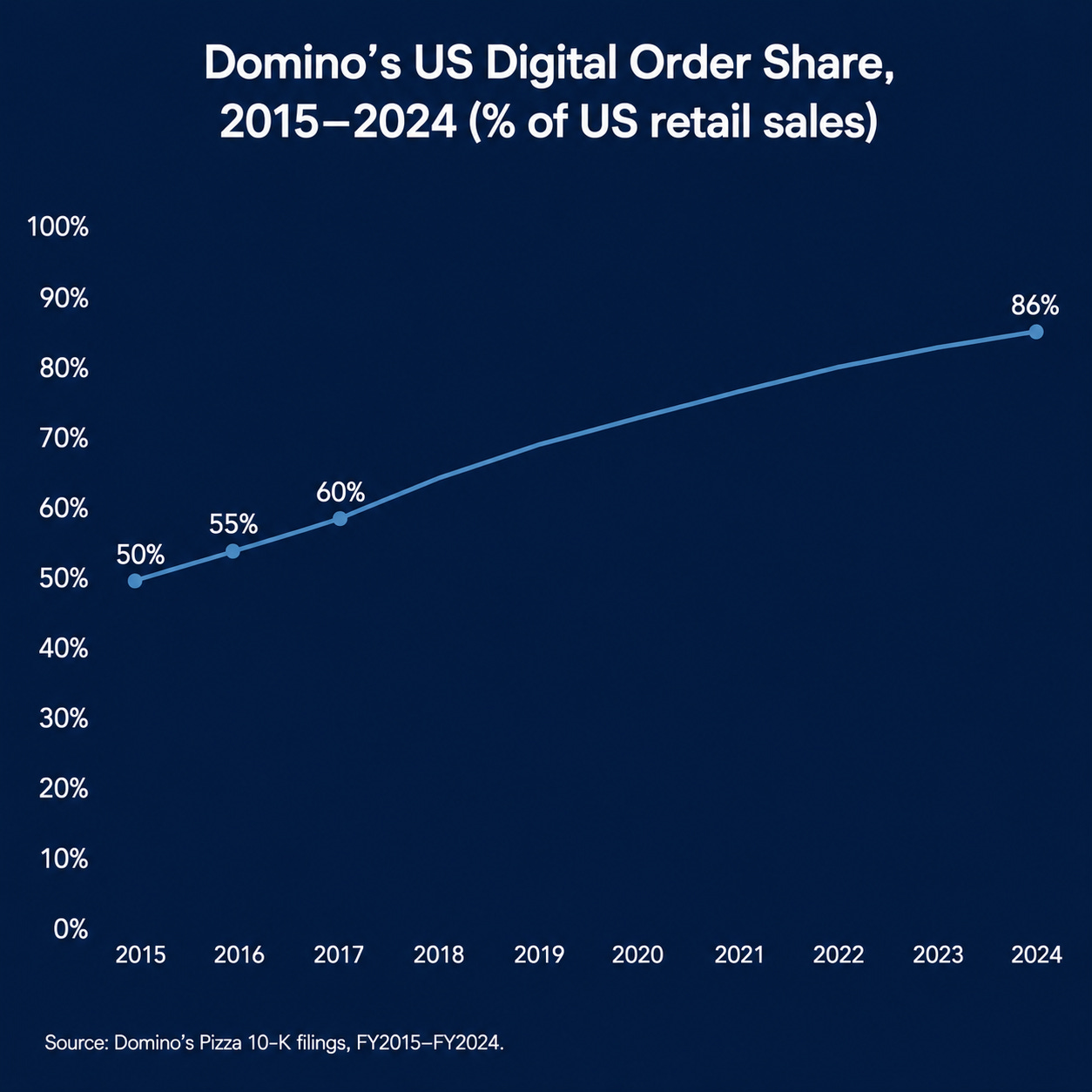

By 2015, digital orders had crossed a threshold Domino’s would record in its own filings:

“In 2015, approximately 50% of our U.S. sales came via digital platforms.”

The following year, the figure crossed “more than half” of US sales again — the language the company used in both its fiscal 2016 and fiscal 2017 annual reports — while global digital sales reached approximately $5.6 billion in fiscal 2016.

In 2016 and 2017, as UberEats, DoorDash, and Grubhub were signing restaurant partners across the industry, Domino’s explicitly declined to join third-party delivery platforms. The stated rationale centered on unit economics and data ownership — Domino’s did not want to pay commission structures on orders it was already fulfilling through its own infrastructure, and it did not want to cede the customer data those transactions would generate. From inside a company that had been building owned delivery infrastructure for decades and had just crossed 50% digital order share, the decision was consistent. From outside, it looked like a company leaving distribution on the table.

The Constraint Layer

To understand what Domino’s had built by 2018, it helps to understand what a competitor would have needed to build to replicate it — and why replication was not simply a capital question.

The platform. Domino’s proprietary digital ordering platform was not a licensed technology stack. It was built internally, maintained internally, and had accumulated data on delivery customer behavior across millions of transactions over nearly a decade. By fiscal year 2015, Domino’s was describing itself as among the largest e-commerce retailers in the United States in terms of annual transactions. A competitor seeking to build a comparable platform would be starting without that data history, without the internal engineering capability to build and iterate on the platform, and without the ordering surface area that Domino’s had spent years extending. A licensed platform from a vendor could replicate the interface. It could not replicate the data, the institutional engineering knowledge, or the integration depth across fifteen-plus ordering surfaces.

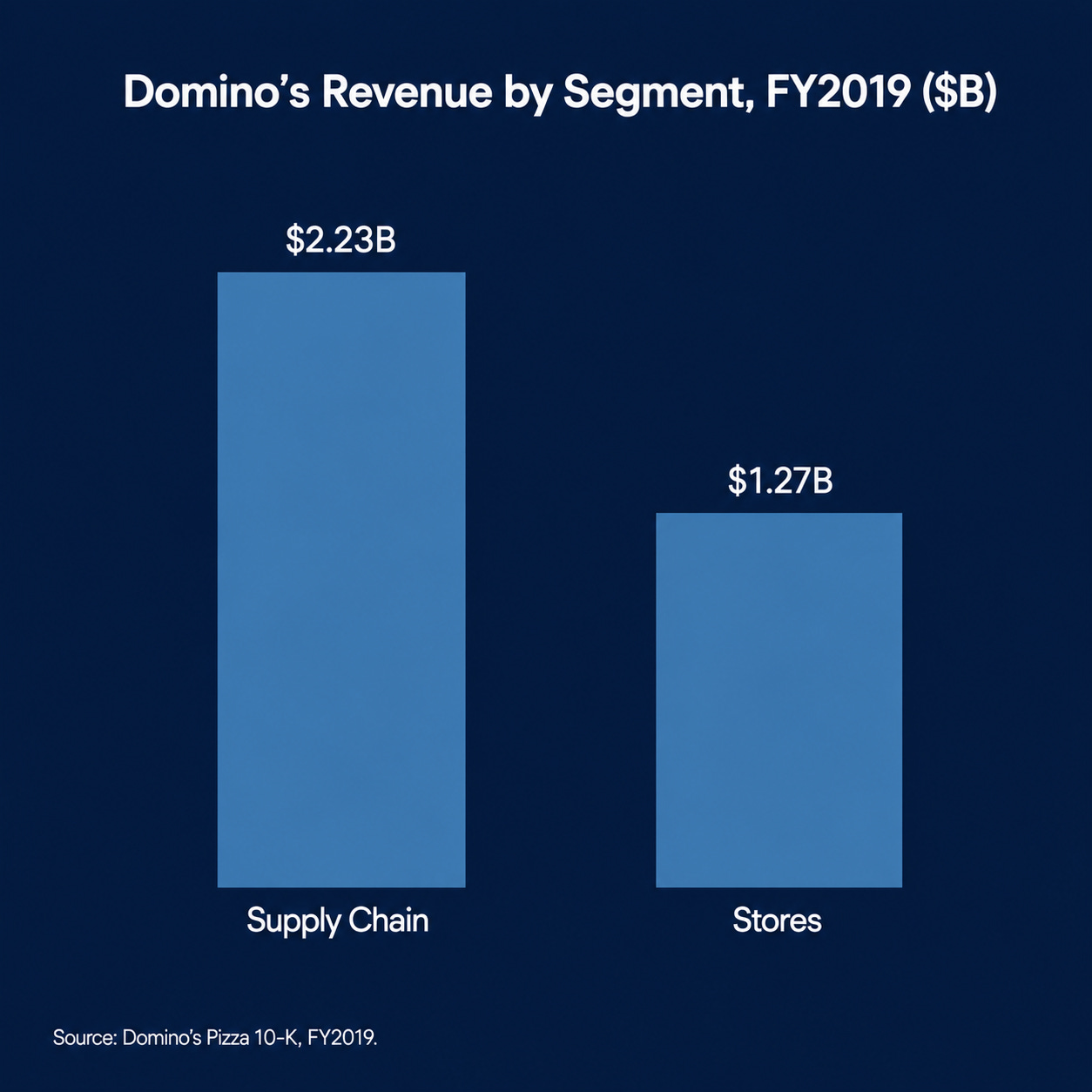

The supply chain. Domino’s owned and operated its supply chain — dough manufacturing facilities, distribution centers, delivery to franchise locations. By fiscal year 2019, supply chain revenues were $2.23 billion, making it the largest single revenue segment in the company’s financials, exceeding the Stores segment at $1.27 billion. The supply chain gave Domino’s cost visibility and quality control that competitors operating through third-party food distribution lacked. It also generated revenue that funded further infrastructure investment. A competitor replicating this position would need to build manufacturing and distribution infrastructure from scratch, at cost, with no revenue offset during the build period.

The franchisee economics. Domino’s franchisees operated on unit economics that had been optimized around owned delivery before the delivery economy arrived. That optimization ran through the supply chain: because Domino’s manufactured and distributed food to its own franchise locations, improvements in supply chain efficiency translated directly into franchisee cost structure — lower food costs, consistent quality, predictable delivery schedules. Corporate investment in supply chain infrastructure was not separable from franchisee profitability. They moved together. Average unit volumes were, by Domino’s chief executive Russell Weiner’s own characterization on an earnings call, better than any primary competitor at nearly $1.4 million annually. When third-party platforms began approaching restaurant franchisees across the industry in 2016 and 2017, Domino’s franchisees had a specific financial reason to resist: their existing system was already working. A competitor seeking to build comparable franchisee alignment would need to simultaneously improve unit economics and persuade franchisees to absorb the capital cost of building owned delivery infrastructure — while those franchisees were being offered what looked like an easier path through platform partnerships.

The data position. Every order placed through Domino’s proprietary platform generated data that Domino’s owned: customer identity, order history, delivery address, delivery time, driver routing, reorder patterns. At 50% digital order share in 2015, rising to more than half across both US and global sales by 2016 and 2017, Domino’s was accumulating this data at a rate no competitor in the pizza category could match. The data informed menu decisions, promotional targeting, driver routing optimization, and delivery radius management. It also made each subsequent order easier to fulfill, which reinforced digital order share, which generated more data. The loop was self-reinforcing, and it had been running for years before competitors recognized it as a competitive variable.

The identity constraint on competitors. The organizational identity Domino’s had built — explicitly a technology company, not a pizza company — was not merely a reputational claim. It determined what the company hired for, what it measured, and what it treated as competitively significant. A restaurant chain that had built its identity around food quality, dining experience, or brand prestige would face an organizational identity problem in attempting to replicate Domino’s position: it would need to become a different kind of company, not merely make a capital investment. Papa John’s, Pizza Hut, and the broader casual dining category entering delivery were not facing a technology gap alone. They were facing a gap in what they believed they were competing for.

None of these five dimensions closed independently. The platform was valuable because the data was deep. The data was deep because digital order share was high. Digital order share was high because the platform was good and the ordering surface was wide. The franchisee economics worked because the owned delivery infrastructure was already built. The owned delivery infrastructure was sustainable because supply chain revenues funded it. Each element supported the others. A competitor entering any single dimension would find the others already defended.

The Compression

The compression, in the Domino’s case, runs in reverse. It did not narrow options — it foreclosed competitor options as it accumulated.

In 2018, Domino’s surpassed Pizza Hut globally to become the largest pizza company in the world by sales. International store count exceeded US store count for the first time. The company had operated through a period of consistent same-store sales growth, rising average unit volumes, and expanding digital order share — all while carrying significant long-term debt from its recapitalization history and returning cash to shareholders through share repurchases. The capital allocation pattern was consistent with a management team that believed the infrastructure was already built and the returns were arriving.

Then, in 2020, the environment Domino’s had been building for arrived all at once.

COVID-19 accelerated delivery adoption across the restaurant industry by several years. Consumers who had previously dined in or carried out shifted to delivery under lockdown conditions. Third-party delivery platforms — UberEats, DoorDash, Grubhub — experienced volume increases that transformed them from startup-phase experiments into essential infrastructure for restaurants that had no owned delivery capability. Restaurants across every category signed platform agreements under conditions of urgency, absorbing commission structures that DoorDash’s own earnings calls described as typically 20 to 30 percent of an order — a cost structure that, for restaurants operating on single-digit margins, consumed most or all of the profit on each delivery transaction.

Domino’s operated through its existing infrastructure — no platform dependency to build, no commission structure to absorb, no urgent logistics problem to solve. Where competitors were encountering the delivery economy as a crisis, Domino’s was encountering it as confirmation. Restaurants that had signed with third-party platforms reported margin compression that Domino’s franchisees were not carrying. Third-party platforms reported significant per-order losses as they competed for market share, raising the question of what restaurant economics would look like when platform pricing reached its equilibrium. Domino’s franchisees were already there — and doing so with unit economics the platform model was structurally unable to match.

In 2023, Domino’s announced a limited partnership with Uber Eats — structured as carryout order visibility rather than delivery outsourcing, framed internally as incremental customer acquisition. Domino’s was using a third-party platform as a customer discovery channel while retaining the delivery relationship, the transaction data, and the per-order economics on the fulfillment side. It was the opposite of the arrangement most restaurant chains had accepted under urgency in 2020.

By fiscal year 2024, more than 85% of Domino’s US retail sales were generated through digital channels. The platform that started as an internal technology team of 150 in 2009 had become the primary surface through which the business ran.

What Domino’s Built

The standard framings of the Domino’s story do not survive contact with the structural record.

It was a turnaround story. The recipe change produced a real and necessary improvement in consumer perception. Same-store sales in Q1 2010 increased 14.3% — a genuine inflection point in consumer response. But a turnaround implies a return to a prior state. Domino’s did not return to anything. It built a position that did not exist before the decade of investment that followed the recipe change. The turnaround framing accounts for 2010. It does not account for 2020.

It was a technology story. The digital platform and the Anyware integrations are real and significant. But describing Domino’s as a technology company mislocates the advantage. The technology was valuable because it was embedded in owned delivery infrastructure, franchisee economics, and supply chain integration that no technology investment alone could replicate. A technology company can be disrupted by a better technology. Domino’s position required disrupting the supply chain, the franchisee network, the data history, and the delivery infrastructure simultaneously.

It was a management story. Patrick Doyle’s leadership was consequential — the conviction that the delivery relationship was the competitive asset, held consistently over a decade, governed the decisions that accumulated the advantage. But the advantage is structural, not personal. It persists beyond any individual’s tenure because it is embedded in the economics of 6,000-plus franchise locations and the data history of hundreds of millions of digital transactions.

What Domino’s actually built was a closed loop. The customer ordered digitally, generating data Domino’s owned. The order was fulfilled by a driver working within a system the franchisee owned and had optimized. The food arrived from a supply chain Domino’s manufactured and distributed. The franchisee’s unit economics made the system worth defending. The data made the next order easier. The loop ran, largely unobserved, for a decade before the environment arrived that made it legible.

The delivery economy did not create Domino’s advantage. It revealed it.

Discussion Question

Domino’s built its structural position during a window when the decisions looked like operational overhead, marketing experiments, or stubbornness — before the delivery economy made them legible as competitive investments. Leadership held a conviction about where competitive advantage would be located in a world that had not yet arrived, and allocated capital consistently with that conviction for nearly a decade before the bet was confirmed.

What would a competitor need to believe about the future of delivery to justify the investment required to close the gap today — and is there any evidence that belief is forming?

If you have a view on this, I’d like to hear it. Leave a comment below.

The podcast version is available wherever you listen to podcasts or at deliberatedriftpodcast.com