Costco: The Membership Fee Looked Like a Gimmick

How a warehouse retailer built a structural position that made the product margin almost irrelevant.

In 1983, a warehouse opened in Seattle and charged people money to shop there. The fee was $25 a year. The idea was not new — Sol Price had been doing it in San Diego since 1976 — and the logic was straightforward: charge members upfront, use the revenue to subsidize lower merchandise prices, give members a reason to come back. It was a funding mechanism. A way to make the math work.

Forty years later, Costco Wholesale Corporation collects approximately $4.8 billion in membership fees annually. Its merchandise operations — the warehouses, the pallets, the $1.50 hot dogs, the Kirkland olive oil — produce almost no profit on their own. The fees are not subsidizing the merchandise. The merchandise is justifying the fees.

That inversion did not happen by accident, and it did not happen quickly. It accumulated through a series of decisions that looked, at the time, like operational discipline. Thin margins. Limited product selection. Unusually high wages for retail workers. No advertising. Each of these looked like a constraint the company had accepted, or a risk it was running. What they were actually doing, in combination and over time, was building an asset that competitors could not replicate — not because the structure was secret, but because replication required accepting years of sub-market returns while waiting for something that only time could produce.

The System

The warehouse club model that Costco inherited from Price Club rested on a specific exchange. Members paid an annual fee. In return, they received access to merchandise priced at margins thin enough that the savings, over a year of shopping, would more than cover the cost of membership. The fee was the entry price. The value proposition was the spread between Costco’s prices and what the member would otherwise pay.

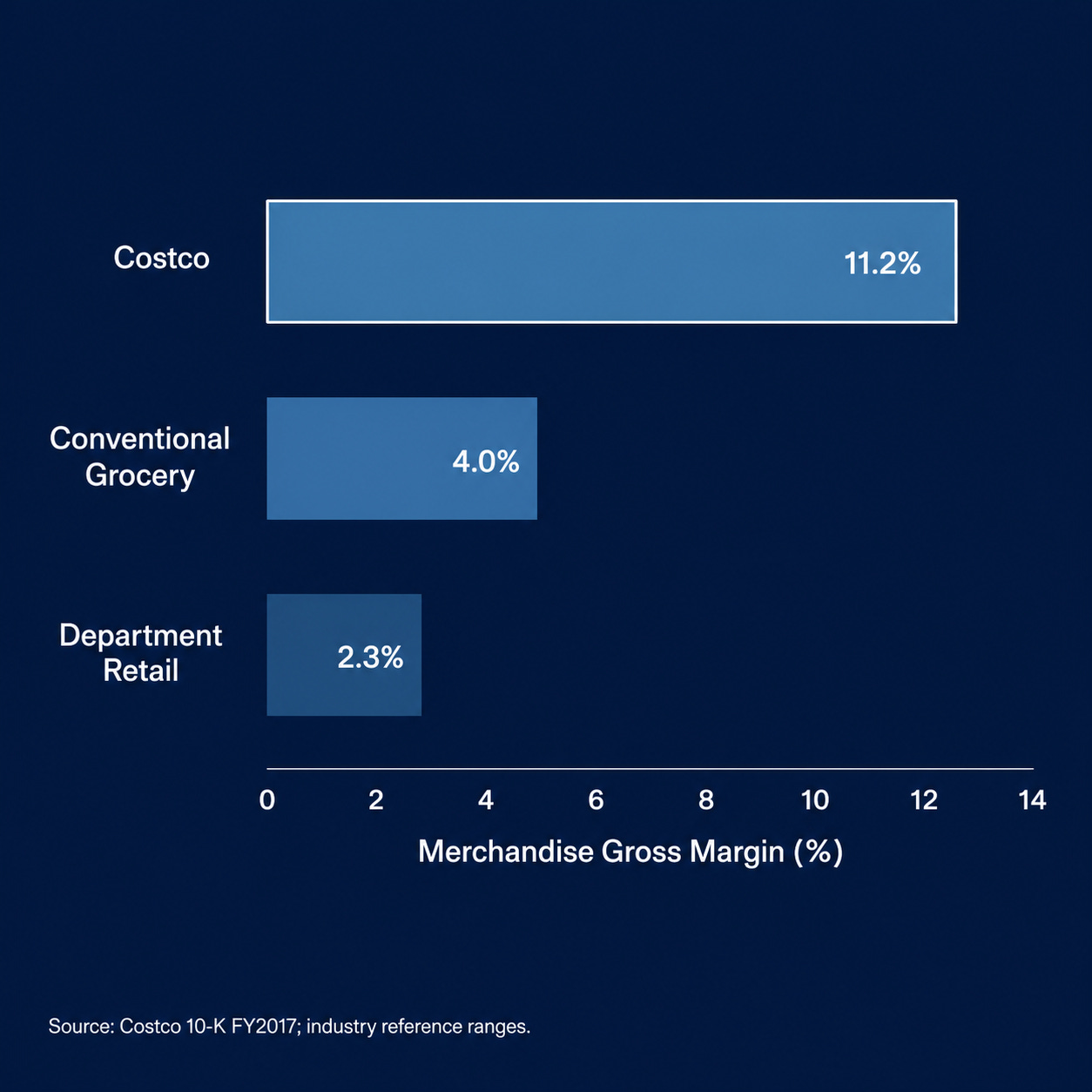

This required Costco to keep merchandise gross margins deliberately low — in the range of 10 to 14 percent, compared to 25 to 30 percent for conventional grocery and considerably more for department retail. The 10-K filings from the early years document this consistently. Costco was not failing to extract margin from its suppliers; it was choosing not to. The margin that a conventional retailer would have kept was being returned to members in the form of lower prices.

The model required one condition to function: members had to believe the fee was worth paying. As long as that belief held, the fee revenue was stable, and stable fee revenue made the thin merchandise margins viable. The whole structure rested on member satisfaction — not as a nice-to-have, but as a load-bearing element.

What made this more than a clever pricing strategy was what happened when members renewed. A member who paid $25 in year one and returned in year two had already decided the exchange was worth it. The second renewal required less persuasion than the first. The third less than the second. Each renewal cycle, the decision to pay shifted incrementally from an evaluation to a habit. The fee became a standing commitment rather than an annual deliberation.

This dynamic was present from the beginning. It was not yet understood as the structural core of the business.

The Shift

The Price Club merger in October 1993 created PriceCostco, a combined entity with more than 200 warehouse locations across the United States, Canada, and several international markets. Jim Sinegal became chief executive of the combined company. The Price family, who had built the original warehouse club concept, exited management within a year. By 1997, the PriceCostco name was retired and all locations rebranded as Costco.

The merger is significant not because of its scale — though the combined buying power mattered — but because of what it required Sinegal to defend. PriceCostco was publicly traded from its formation. Quarterly earnings pressure was now structural. Analysts covering the company could see that Costco was sitting on merchandising scale it was not monetizing. The question, asked consistently through the mid-1990s and into the 2000s, was straightforward: why not expand margins?

Sinegal’s answer was always the same. Expanding merchandise margins would damage the value proposition members were paying to access. If the prices rose toward conventional retail levels, the fee stopped making sense. Members who stopped believing the fee was worth it would not renew. And if they did not renew, the fee revenue that made the thin merchandise margins viable would erode. The merchandise margin cap — held below 15 percent, and in most years well below — was not operational conservatism. It was the mechanism by which the membership asset was being built.

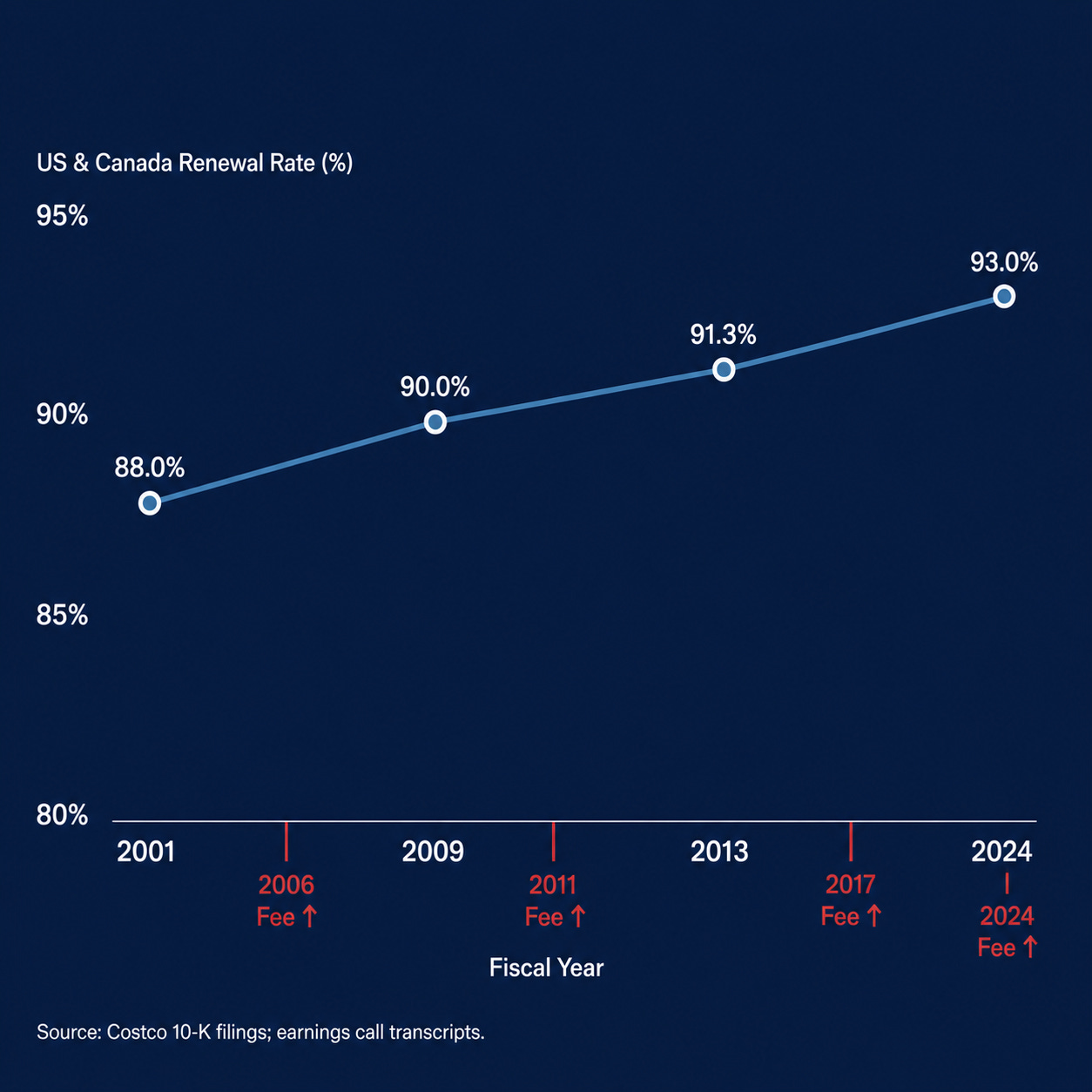

The discipline held. And it outlived him. On a Q3 FY2024 earnings call, decades after the original margin defense was first articulated, analyst Chuck Grom of Gordon Haskett put the question to current CEO Ron Vachris directly: the 14 to 15 percent margin ceiling had been in place for years — did Costco intend to maintain it? Vachris answered without equivocation. That ceiling, he said, had been part of how Costco measured return for many years. There were no plans to move it.

The question had been asked, in various forms, for three decades. The answer had not changed. What was shifting during this period, largely beneath the surface of the financial reporting, was the quality of the membership base. Each year that a member renewed was a year in which the renewal decision moved further from a price comparison and closer to an automatic commitment. The base was not just growing. It was maturing.

The Response

Competitors watched Costco’s growth and drew the obvious conclusion: the warehouse club format worked, and scale was the route to competing in it. Sam’s Club, operating within Walmart’s structure, expanded aggressively through the 1990s and 2000s. BJ’s Wholesale Club established a regional presence in the Northeast. Both followed the same basic template — large-format warehouse, membership fee, limited SKU count, bulk merchandise.

Neither closed the gap with Costco on the metric that mattered most.

Sam’s Club’s membership renewal rates have consistently trailed Costco’s by a significant and persistent margin — a gap documented in analyst and industry coverage across multiple decades. The structural reason is not difficult to identify. Sam’s Club operates within Walmart, which means its financial performance is reported as part of a consolidated enterprise with its own earnings expectations. Holding merchandise margins at Costco’s floor — accepting near-zero merchandise profit in exchange for membership asset accumulation — is a commitment that a standalone operator can sustain more easily than a division of a publicly traded conglomerate whose shareholders are measuring consolidated returns. Sam’s Club could replicate Costco’s format. It could not fully replicate Costco’s incentive structure.

BJ’s faced a different version of the same problem. A regional operator building a membership base from scratch in the 2000s was not just competing against Costco’s current value proposition. It was competing against the accumulated renewal history of a membership base that had been renewing for twenty years. A new member at BJ’s was making a first-year decision. A member renewing at Costco for the fifteenth time was not.

The responses confirmed rather than disrupted Costco’s position. Format replication without operational replication produced a weaker version of the model. And operational replication without temporal replication — without the years of renewal history that produced habituated behavior — produced a membership base that had not yet developed the inertia that Costco’s had.

The Accumulation

Three reinforcing mechanisms were operating simultaneously through the 2000s and into the 2010s, each compounding the others.

The first was the renewal flywheel. Thin merchandise margins delivered genuine value, which produced high renewal rates, which produced stable fee revenue, which funded continued investment in buying power and employee quality, which sustained the value that produced high renewal rates. Each cycle of this loop did not just maintain the position — it deepened it. Members who had renewed multiple times were not evaluating Costco against alternatives each year. The evaluation had already occurred, repeatedly, and the answer had been the same each time. The renewal was becoming automatic.

The second was the stock-keeping unit (SKU) trust loop. Costco’s warehouses carry fewer than 4,000 active SKUs. A conventional supermarket carries tens of thousands. The constraint is also a service: because Costco selects so few products, the selection itself is a curation signal. A member who trusts Costco’s judgment about which olive oil or which mattress to carry does not need to comparison shop. That trust accumulates with each satisfactory purchase. The Kirkland Signature private label, expanding steadily through this period, deepened the loop further. A household that relies on Kirkland for a meaningful portion of its regular purchasing has built a dependency that does not dissolve when the membership fee increases by five dollars.

The third was the employee quality loop. Costco has paid above-market wages for retail workers since its founding — a policy that drew consistent analyst criticism on cost grounds and was defended by management on retention grounds. The Q4 FY2024 earnings call documents average US and Canada wages just above $30 an hour. The structural consequence of above-market compensation is lower turnover. Lower turnover produces more experienced warehouse staff. More experienced staff produces more consistent member experience. Consistent member experience is a component of the renewal value proposition. This loop operates on a longer cycle than the others, but its output — the institutional knowledge and service consistency embedded in a stable workforce — is the hardest element of the model for a competitor to replicate, because it requires sustained above-market labor investment for years before the benefit compounds into measurable renewal behavior.

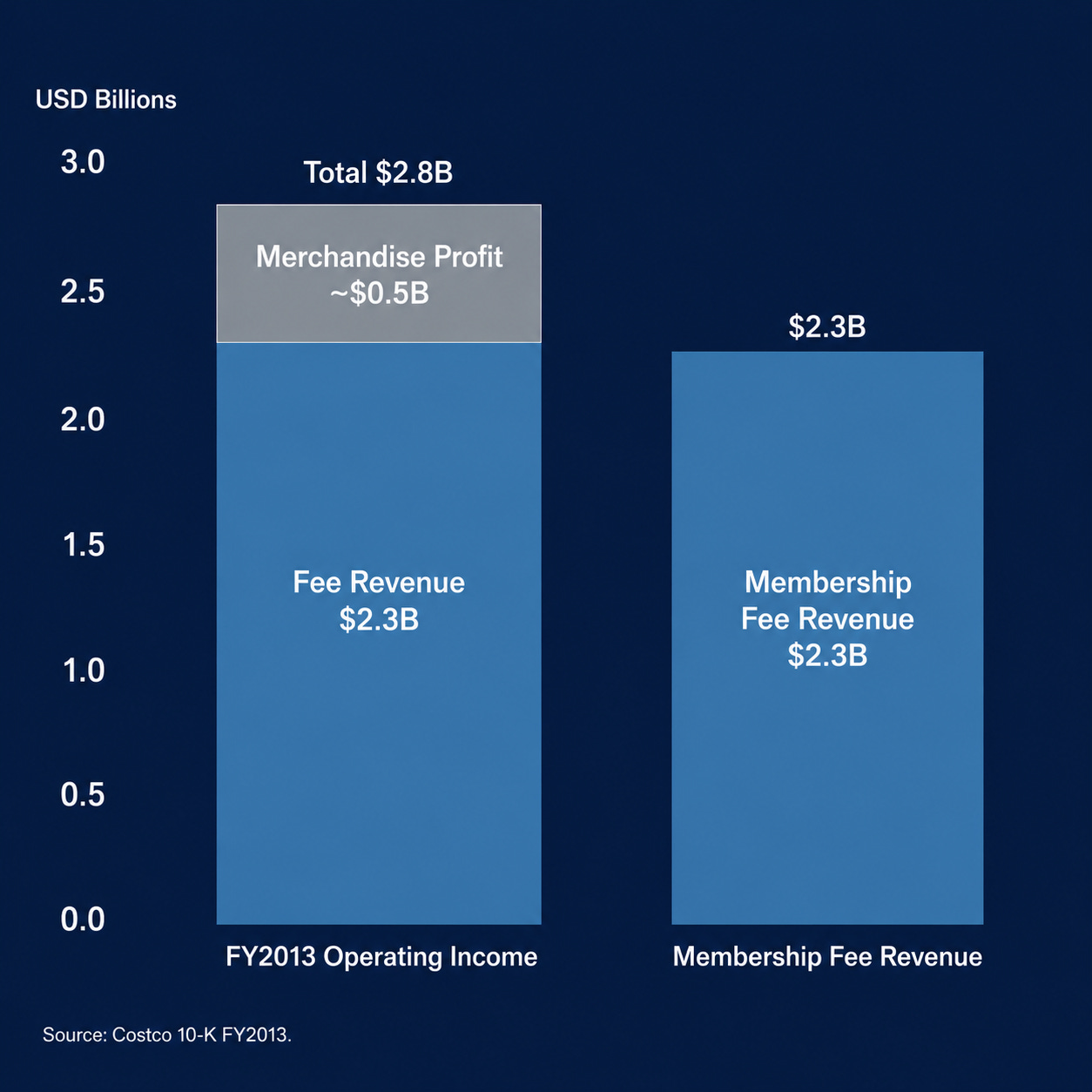

By fiscal year 2013, the structural consequence of these three loops running simultaneously for two decades was visible in Costco’s income statement. Membership fee revenue came in at approximately $2.3 billion. Operating income came in at approximately $2.8 billion. The merchandise operations — the warehouses, the inventory, the supply chain, the employees — produced operating profit of roughly $500 million on net sales exceeding $100 billion. The fee revenue was not supplementing the merchandise profit. It was the profit. The merchandise existed to justify the renewal.

The Lock-In

The temporal barrier is the one that cannot be purchased. A competitor entering the warehouse club market in 2013 could raise capital, build warehouses, hire buyers, and price merchandise at thin margins. What it could not do was compress the years required for a membership base to mature from deliberate evaluation into habitual renewal. That compression is not available at any price.

The other requirements follow from it: establishing a sufficient initial membership base to fund operations at thin merchandise margins; delivering enough value, consistently enough, over enough renewal cycles to begin producing habituated behavior; sustaining above-market labor costs before the retention benefit appears in the service quality data; building a private label brand from zero against a Kirkland Signature that had been a household staple in millions of homes for fifteen or twenty years. None of these is individually impossible. In combination, over the time horizon required, they constitute a commitment that no publicly traded competitor has demonstrated the organizational capacity to sustain. The barrier is not capital. It is time — and the organizational discipline required to accept below-market returns while time does its work.

The membership asset is not a list of names and credit card numbers. It is a behavioral state — the accumulated habit of renewal across millions of households. A member renewing for the first time is making a deliberate cost-benefit evaluation. A member renewing for the twelfth time is largely not. The fee has been absorbed into the household budget. The shopping pattern has been established. The switching cost is not the annual membership fee — it is the disruption of a deeply embedded routine.

Sam’s Club, which opened its first location in 1983, has operated the same warehouse club format for as long as Costco. In fiscal year 2024, Costco’s US and Canada membership renewal rate was 92.9 percent. The gap between the two companies is not a gap in execution. It is a gap in accumulated time, organizational incentive alignment, and the depth of habituated renewal behavior those two things produce.

The Compression

The fee increase in September 2024 — from $60 to $65 for Gold Star membership and from $120 to $130 for Executive membership, the first increase in seven years — was the most direct test of the structural position Costco had built. A fee increase is an explicit request for members to reaffirm the value proposition. A membership base that is renewing out of habit rather than current-period evaluation absorbs the increase without significant attrition. A membership base that is still making annual price comparisons does not.

The Q4 FY2024 earnings call documents the result. US and Canada renewal rate: 92.9 percent. Worldwide: 90.5 percent. CFO Gary Millerchip, responding to analyst questions about member attrition, stated that the company had not seen a significant member reaction and that renewal rates remained stable.

The minor decline in the US renewal rate — down 0.1 percentage points from the prior quarter — was attributed specifically to a 2023 digital promotion that had generated more than 200,000 new sign-ups. Digital promotions attract a younger, less habituated cohort that renews at a lower initial rate. As that cohort entered the renewal calculation, it dragged the aggregate rate down marginally. The underlying renewal behavior of the established base was unchanged.

The fee increase is not just a revenue event. It is a measurement. Each time Costco raises the fee and absorption is confirmed, the structural durability of the membership asset is documented. The 2006 increase was absorbed. The 2011 increase was absorbed. The 2017 increase was absorbed. The 2024 increase was absorbed. The pattern is not a coincidence. It is the accumulated result of two decades of delivered value compounding into behavioral lock-in.

Costco entered fiscal year 2025 with 76.2 million paid household members. At the current fee levels, the annual fee revenue run rate exceeds $4 billion. That revenue is largely independent of merchandise sales fluctuations, largely immune to the margin compression dynamics that govern conventional retail competition, and largely secured by behavioral inertia that has been compounding for forty years.

What Costco Built

Three framings of Costco’s position are common, and all three miss the structural point.

The first is that Costco succeeds because of scale. Scale matters — purchasing leverage is real, and operating a high-volume warehouse efficiently requires genuine capability. But scale alone does not explain a 92.9 percent renewal rate. Walmart has more scale than Costco. Sam’s Club has been running the same format for as long. Scale is a necessary condition for the model. It is not the structural advantage.

The second is that Costco succeeds because of operational discipline — the margin cap, the SKU restraint, the refusal to advertise. The discipline is real and has been maintained against persistent pressure. But discipline is a behavior, not an asset. What the discipline produced over time — the membership base whose renewal behavior has become habitual — is the asset. Costco is not valuable because its management is disciplined. Its management has been disciplined long enough that the result of the discipline has become self-sustaining.

The third is that Costco succeeds because members love it. Customer satisfaction scores are consistently high. The brand generates genuine affection. But affection is not a structural position. What looks like affection from the outside is, in structural terms, the behavioral expression of accumulated switching costs. Members do not renew at 92.9 percent because they are enthusiastic. They renew because the renewal has become automatic — because the shopping pattern is established, the private label dependencies are real, and the disruption cost of switching exceeds any plausible benefit from doing so.

What Costco actually built is a revenue stream that does not behave like retail revenue. It does not fluctuate with consumer sentiment in the way merchandise sales do. It does not compress under competitive pricing pressure. It does not require quarterly promotional investment to sustain. It compounds — not dramatically, not visibly, but year over year, renewal cycle by renewal cycle, as the membership base matures and the habit deepens.

The 2009 financial crisis tested this. Through a period of significant consumer spending contraction, Costco’s renewal rates held. The Q2 FY2009 earnings call documents the US and Canada renewal rate at approximately 87.5 percent — in the middle of the worst consumer spending environment in a generation. Merchandise sales declined. Fee revenue did not.

That durability is not a product feature. It is the structural output of twenty-five years of operational decisions that, taken individually, looked like restraint, and taken together, built something that conventional retail analysis had no framework to value.

DISCUSSION QUESTION

Costco’s renewal rates have held above 90 percent through recessions, fee increases, and the expansion of digital retail alternatives. The warehouse experience — the limited selection, the discovery dynamic, the physical scale — continues to justify the fee for the overwhelming majority of members who encounter it.

The experience that produces renewal is a physical one. It depends on members showing up, navigating the warehouse, encountering products they did not plan to buy. That is what the Kirkland brand is built on. It is what makes Costco structurally different from a subscription service that delivers boxes to a door.

The question the structural analysis opens, but does not resolve, is this: at what point does the shift in consumer behavior toward digital purchasing begin to erode the warehouse visit frequency that the renewal motivation depends on — and whether Costco’s response to that shift, when it becomes necessary, will require changes to the model that the model’s own incentive structure makes difficult to make?

If you have a view on this, I’d like to hear it. Leave a comment below.

The podcast version is available wherever you listen to podcasts or at deliberatedriftpodcast.com